US and Canadian banks were closed for the holiday, but that didn’t stop some asset classes like crude oil and Bitcoin from making volatile moves.

Here’s what’s driving the markets so far.

Titles:

- On Friday after the market closes The Standing Committee of the National People’s Congress confirmed 10 trillion yuan ($1.4 trillion) to allow local governments to reduce their “hidden” debt.

- on saturday, China recorded a CPI reading of 0.3% year-on-year For October (0.4% expected, 0.4% prior) – slowest gain in four months

- Producer price index in China Decreased by 2.9% y/y in October (-2.5% expected, -2.8% previously)

- Summary of the Bank of Japan’s deliberations The bank discussed the need to be cautious in raising interest rates, and remained vague about its December move

- Japan’s current account surplus narrowed from JPY 3.15 trillion to JPY 1.27 trillion (JPY 2.80 trillion expected)

- New Zealand quarterly inflation expectations For the next two years, from 2.03% to 2.12% in the third quarter of 2024.

- New Chinese loans Slowed from CNY 1,590 billion to CNY 500 billion in October (expected CNY 770 billion)

- Japan’s economic sentiment index fell from 47.8 to 47.5 (expect 47.2) in October

- French, Canadian and American banks closed their doors on the occasion of their holidays

Broad market price movement:

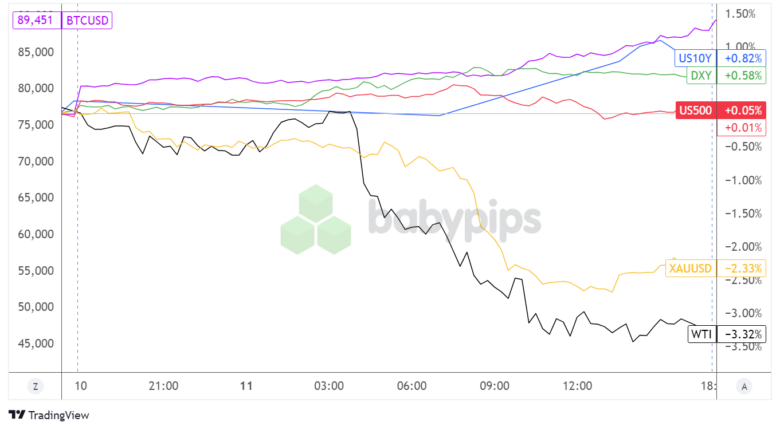

Dollar index, gold, S&P 500, oil, US 10-year yield, Bitcoin overlay Chart by TradingView

Commodities such as gold and crude oil had a tough Monday, with the former finishing down more than 2% for the day while the latter posted losses of more than 3%, likely in reaction to weak Chinese inflation data released over the weekend and the market continuing. Disappointment with the country’s stimulus efforts.

Bitcoin bulls, on the other hand, were having the time of their lives as the BTC/USD price soared to new highs crossing the $89K mark in anticipation of cryptocurrency-friendly regulations during the Trump administration.

US bond markets were closed on Veterans Day, but 10-year bond yields remained higher while the S&P 500 closed flat.

Forex market behavior: US dollar against major currencies:

Overlay of the US dollar against major currencies Chart by TradingView

Data flow was light on Monday, with only a few mediocre reports such as New Zealand’s quarterly inflation expectations report and China’s new loan data. This set the stage for mostly sideways price action early in the day, before the US dollar’s general shift higher near the London session.

The yen was noticeably weaker against the dollar throughout the day, as minutes from the Bank of Japan’s monetary policy meeting released over the weekend revealed that officials preferred to be cautious about tightening moves and refrained from dropping hints about a rate hike in December.

The euro also suffered losses at the start of the week, with political uncertainty in Germany weighing on the shared currency, along with another set of potential trade disputes with the United States during a Trump presidency.

Potential catalysts coming on the economic calendar:

- Initial machine tool orders in Japan at 6:00 AM GMT

- Number of claimants in the UK, unemployment rate and average income index 7:00 AM GMT

- Bank of England Monetary Policy Committee member Hugh Bell’s speech at 9:00 AM GMT

- German and Eurozone ZEW economic sentiment indicators at 10:00 AM GMT

- FOMC Member Waller’s speech at 3:00 AM GMT

- FOMC Member Barkin’s speech at 3:15 PM GMT

- FOMC Member Kashkari will speak at 7:00 PM GMT

- FOMC Member Harker’s speech at 10:00 PM GMT

- Japan Producer Price Index report at 11:50 PM GMT

There could be an impact from sterling volatility later today, as the UK prepares to print the latest employment data, which could then impact the Bank of England (BOE) policy outlook.

After that, focus will likely shift to the US dollar as a number of FOMC officials line up to testify and perhaps offer hints about the central bank’s future moves.

Check out our brand new Forex Correlation Calculator if you plan on making any trades!

Comments are closed, but trackbacks and pingbacks are open.