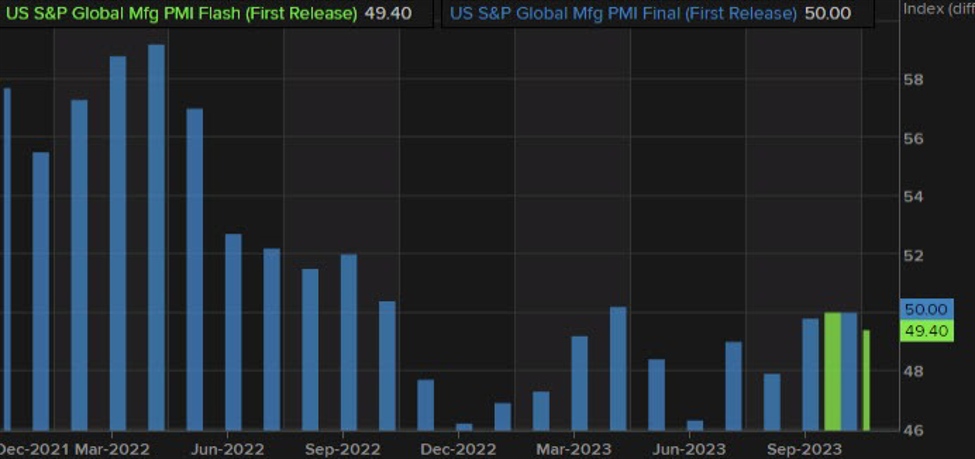

S&P Flash manufacturing PMI remains below 50.0

- Prior PM Mfg 50.0

- Flash Manufacturing PMI 49.4 vs 49.8 estimate

- Flash services PMI 50.8 vs 50.4 estimate ant 50.6 last month

- Composite 50.7 unchanged from last month 50.7.

From S&P Global:

In November, US businesses experienced a marginal expansion in output, similar to the growth rate seen in October. Both manufacturers and service providers saw a slight increase in activity. Total new orders returned to growth after three months of contraction, but demand conditions for manufacturers remained unchanged.

As a result of subdued demand and decreasing backlogs, companies reduced their workforce for the first time since June 2020, affecting both service providers and goods producers. Cost pressures eased, with input prices rising at the slowest rate in over three years. However, higher service sector output charges contributed to an increase in overall selling price inflation, although manufacturers experienced a slower rise in factory gate charges in November.

Commenting on the data, Siân Jones, Principal Economist at S&P Global Market Intelligence said:

“The US private sector remained in expansionary territory in November, as firms signalled another marginal rise in business activity. Moreover, demand conditions – largely driven by the service sector – improved as new orders returned to growth for the first time in four months. The upturn was historically subdued, however, amid challenges securing orders as customers remained concerned about global economic uncertainty, muted demand and high interest rates. Business uncertainty was also heightened among US firms, as expectations regarding the year-ahead outlook slipped to the weakest

since July.

Businesses cut employment for the first time in almost three-and-a-half years in response to concerns about the outlook. Job shedding has spread beyond the manufacturing sector, as services firms signalled a renewed drop in staff in November as cost savings were sought. “On a more positive note, input price inflation softened again, with cost burdens rising at the slowest rate in over three years. The impact of hikes in oil prices appear to be dissipating in the manufacturing sector, where the rate of cost inflation slowed notably. Although ticking up slightly, selling price inflation remained subdued relative to the average over the last three years and was consistent with a rate of increase close to the Fed’s 2% target.”

ON EMPLOYMENT:

- In November, US companies saw a decline in employment, the first in nearly 3.5 years.

- The decrease affected both the service sector and manufacturers.

- Causes cited for layoffs included subdued demand, high cost pressures, and hiring freezes due to margin concerns.

- Diminishing levels of unfinished business also contributed to the workforce reduction.

- Backlogs of work had been declining for seven consecutive months in the final quarter of 2023.

- Both goods producers and service providers experienced faster contractions in incomplete business, mainly due to reduced operating capacity pressure.

ON INFLATION:

- Margin pressures eased in the private sector.

- Companies raised selling prices more quickly.

- Cost inflation rate slowed for the second consecutive month.

- Input prices continued to rise but at the slowest pace since October 2020.

- Some firms noted lower energy and raw material costs.

- Workforce reduction also contributed to easing cost pressures.

- Manufacturers saw a notable slowdown in input price inflation.

- Service sector firms led a faster rise in overall selling prices in November.

- Manufacturers had the slowest increase in factory gate charges since August.

- The aim was to drive new sales and maintain competitiveness.