It was a BUSY trading day for traders, who saw RBNZ and BOC’s policy decisions AND priced in a hotter-than-expected U.S. inflation read.

How did your favorite assets react to yesterday’s catalysts?

Here’s what you missed from yesterday’s trading:

Headlines:

- RBNZ kept its interest rates at 5.50% and said that a restrictive monetary policy stance “remains necessary”

- Credit ratings agency Fitch affirmed its “A+” rating for China but also adjusted its outlook from “stable” to “negative”

- Italy’s retail sales for February: 0.1% (0.2% forecast, 0.0% previous)

- Canada Building Permits for February: 9.3% m/m C$11.8B (-1.2% m/m forecast; 12.9% m/m previous)

-

The Bank of Canada held its overnight policy rate at 5.00% & continues to normalize its balance sheet

- BOC forecasts GDP growth of 1.5% in 2024, 2.2% in 2025, and 1.9% in 2026

- The Bank expects CPI inflation to be close to 3% during the first half of this year, move below 2½% in the second half, and reach the 2% inflation target in 2025.

- U.S. CPI and Core CPI for March: 0.4% m/m (0.3% m/m forecast; 0.4% m/m previous); Annualized, Core CPI was 3.8% y/y (3.7% y/y forecast) while the headline was noticeably higher at 3.5% y/y (3.4% y/y forecast; 3.2% y/y previous)

- EIA’s crude oil inventories increased by 5.8M barrels per day in the week ending April 5, higher than the expected 0.9M increase and the previous week’s 3.2M uptick

- In a conference, FOMC voting member Thomas Barkin said that it’s “smart” that the Fed is taking its time with the next policy changes

- FOMC’s March meeting minutes noted the members’ “uncertainty about the persistence of high inflation” and that “recent data had not increased their confidence that inflation was moving sustainably down to 2%”

- U.S. government budget deficit narrowed from $296.8B to $236.5B in March (vs. -$209.4B expected)

- Talks of Iran’s “imminent” missile or drone strikes against targets in Israel weighed on overall risk sentiment

- U.K.’s RICS house price balance improved from -10% to -4%; “This suggests a largely stable picture is in place for house prices”

- Australia’s MI inflation expectations rose from 4.3% to 4.6% in April

- China’s annual CPI slowed down from 0.7% to 0.1% (vs. 0.4% expected) in March; PPI slowed further from -2.7% to -2.8% as expected

Broad Market Price Action:

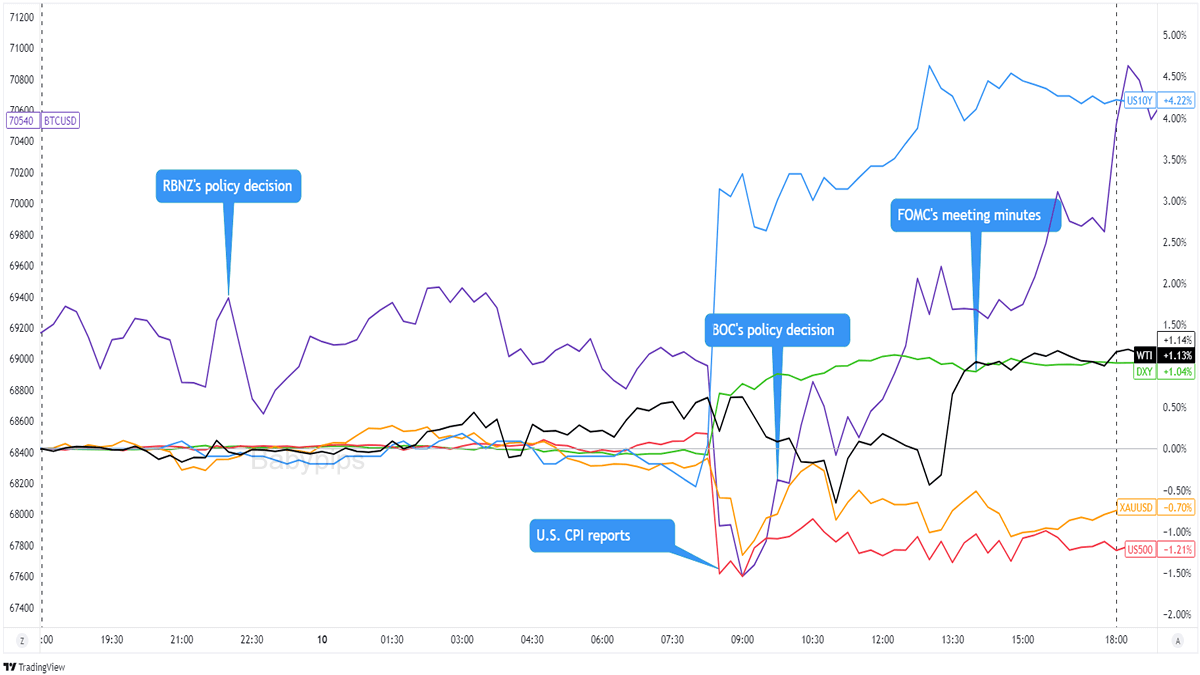

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

The Reserve Bank of New Zealand (RBNZ) started a calendar-heavy trading day when it announced that it’s keeping its interest rates steady at 5.50% in April AND defended that a restrictive policy stance “remains necessary.”

Link to RBNZ’s policy decision details and NZD’s reaction

Volatility was limited to major NZD pairs, however, as other major financial assets traded in tight ranges ahead of the anticipated U.S. inflation reports. In fact, we didn’t see much action until Uncle Sam’s CPI reports came in better than analysts’ estimates in March.

Link to U.S. CPI report details and USD’s reaction

A stronger-than-expected inflation supported a “higher for longer” stance for the Fed and pushed back estimates of the Fed’s next cut. According to the CME FedWatch Tool, September’s odds picked up from 33.7% to 44.9%.

Not surprisingly, U.S. Treasury yields jumped and the U.S. dollar gained at the strong CPI read while “risk” assets like bitcoin (BTC/USD), crude oil, and U.S. stocks traded lower.

The Bank of Canada (BOC) also made headlines when it kept its interest rates at 5.00% as expected but Governor Macklem also said that a June rate cut is “in the realm of possibilities.”

Unfortunately for CAD bulls, traders saw enough optimism in the central bank’s revised growth and inflation forecasts that speculations of a June rate cut actually decreased once the dust settled around the release.

Link to BOC’s policy decision details and CAD’s reaction

The Fed also published its March meeting minutes where we saw more of the members’ uncertainty over the persistence of high inflation. FOMC members were generally not convinced that inflation is moving sustainably down to 2%, and are making room for some unevenness in the monthly data.

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar mostly traded in tight ranges during the Asian and early European trading sessions though we did see some weakness against NZD following a “hawkish hold” event from the RBNZ.

As mentioned above, the Greenback gained support from a hotter-than-expected CPI report that supported a “higher for longer” interest rate environment in the U.S.

The Fed’s meeting minutes showing the members’ uncertainty about a sustainable deceleration for inflation also supported USD but that was after a bit of pullback so the dollar didn’t really make new intraday highs.

USD saw heavy gains against “risky” bets like AUD, NZD, and GBP but also made legit pips against counterparts like EUR, CHF, CAD, and JPY.

Upcoming Potential Catalysts on the Economic Calendar:

- BOE’s credit conditions survey at 8:30 am GMT

- ECB’s policy decision at 12:15 pm GMT (Lagarde’s presser at 12:45 pm GMT)

- U.S. PPI reports at 12:30 pm GMT

- U.S. initial jobless claims at 12:30 pm GMT

- FOMC member John Williams to give a speech at 12:45 pm GMT

- FOMC member Thomas Barkin to give a speech at 2:00 pm GMT

- NZ BusinessNZ manufacturing index at 10:30 pm GMT

- New Zealand’s food price index at 10:45 pm GMT

- China’s trade balance data due in the Asian session

It’s the ECB’s turn under the spotlight today!

Markets see President Lagarde and her team keeping their policies steady in April but also announcing changes to their expectations for future meetings. That means we gotta pay closer attention to the ECB statement AND presser!

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!

Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!