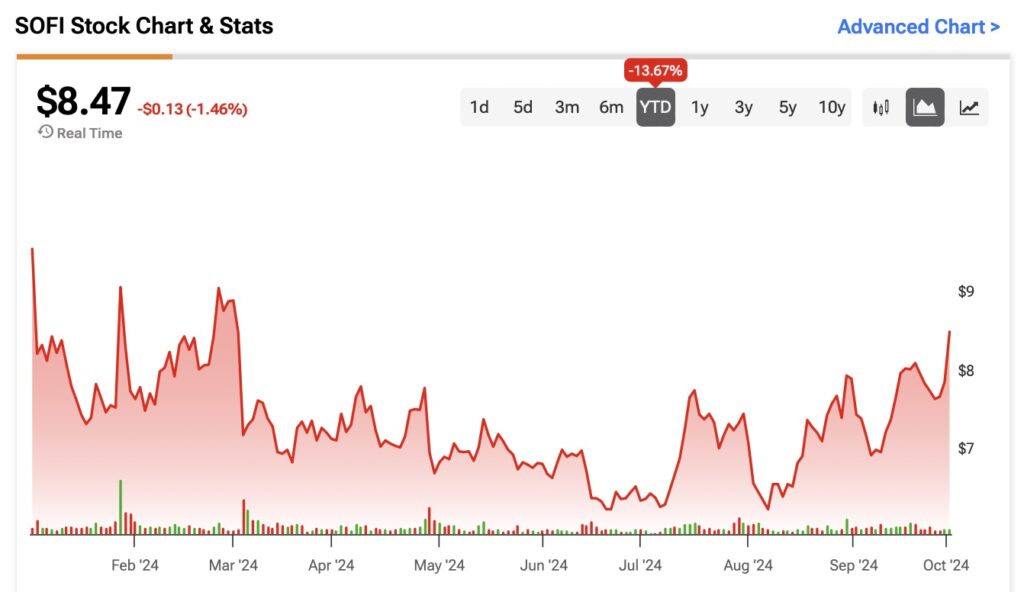

SoFi Technologies (SOFI) has positioned itself as one of the most exciting fintech companies, offering a wide range of services and products that many traditional banks struggle to match. While the stock is down about 10% this year, I believe this decline is largely due to short-term investors being preoccupied with the challenges, especially the high interest rate environment that is now beginning to change. In this article, I will outline five key reasons that support my bullish view on SOFI stock, especially at current levels.

Strong revenue growth and diversification

The first principle of my SoFi investing thesis is its incredible growth. In its most recent second-quarter results, reported on July 30, SoFi posted a solid 22% year-over-year increase in adjusted net revenue, reaching a record $597 million. Furthermore, its financial services and technology platforms revenues grew 46% year over year and now make up 45% of total adjusted net revenues, compared to just 38% last year. This diversification away from lending and toward financial services and technology platforms enhances SoFi’s growth potential and reduces its reliance on a single revenue stream, making the company more resilient.

Additionally, SoFi has created a niche in financial services by targeting a young, high-income demographic that is often underserved by traditional banks. While most major banks offer limited specialized services, SoFi offers a comprehensive range of offerings, from student loans to estate planning, allowing it to meet the specific needs of this demographic.

SoFi improves profitability

In addition to strong revenue growth, SoFi has made significant strides in profitability. The fintech posted three straight quarters of profitability, with $17 million in GAAP net income for the three months ending June 2024, compared to a loss of $40 million a year earlier. This meaningful improvement strengthens investor confidence and demonstrates that SoFi’s business model is sustainable and able to expand profitably over time.

Furthermore, SoFi’s focus on product development, coupled with its commitment to operational efficiency, is poised to drive long-term growth and profitability. Wall Street shares this optimism, forecasting strong earnings growth over the next three years from $0.11 per share in 2024 to $0.64 per share in 2027. This underscores the company’s strong future prospects.

Valuation in line with future growth prospects

The company’s current valuation is also attractive compared to its growth prospects. Currently, SoFi is trading at a forward P/E ratio of 78x. However, if SoFi reaches EPS of $0.64 by 2027, this multiple would drop to 13.4x. This valuation is much closer to that of traditional banks, which typically trade at earnings multiples between 11x and 13x.

However, since SoFi’s business is still far from mature, and earnings are just getting started, the current P/E ratio premium makes sense.

Member growth and digital-first strategy

My fourth upside relates to SoFi’s rapid growth of its member base. In the second quarter of 2024, the company added 643,000 new members, representing a 41% increase year over year, bringing the total to 8.77 million members. SoFi’s digital-first approach also eliminates the need for physical locations and helps reduce costs while meeting consumer demand for convenient, technology-driven financial services. This strategy positions SoFi well to benefit from the ongoing shift toward online banking and innovation in fintech.

Flexible lending business with prudent risk management

The fifth argument behind my bullish view on SOFI is the potential macroeconomic relief. The administration has been concerned over the past few quarters that higher interest rates could dampen economic activity, leading to job losses and missed loan payments. As a result, management aims to reduce lending, initially forecasting a revenue decline of at least 5% for 2024.

However, with the Fed cutting interest rates by half a percentage point a few weeks ago, the administration’s outlook is likely to improve. SoFi may have been spared the worst of the rising interest rate cycle. Lower interest rates usually improve economic activity, reducing the risk of loan losses.

Despite diversification efforts, SoFi’s balance sheet remains heavily concentrated in lending, with a loan-to-assets ratio of about 77.4%. Management’s caution was justified, as an increase in defaults could seriously threaten results. Notably, the 90-day personal loan delinquency rate fell to 64 basis points in the fourth quarter, down from 72 basis points in the first quarter, indicating a potential peak in delinquencies.

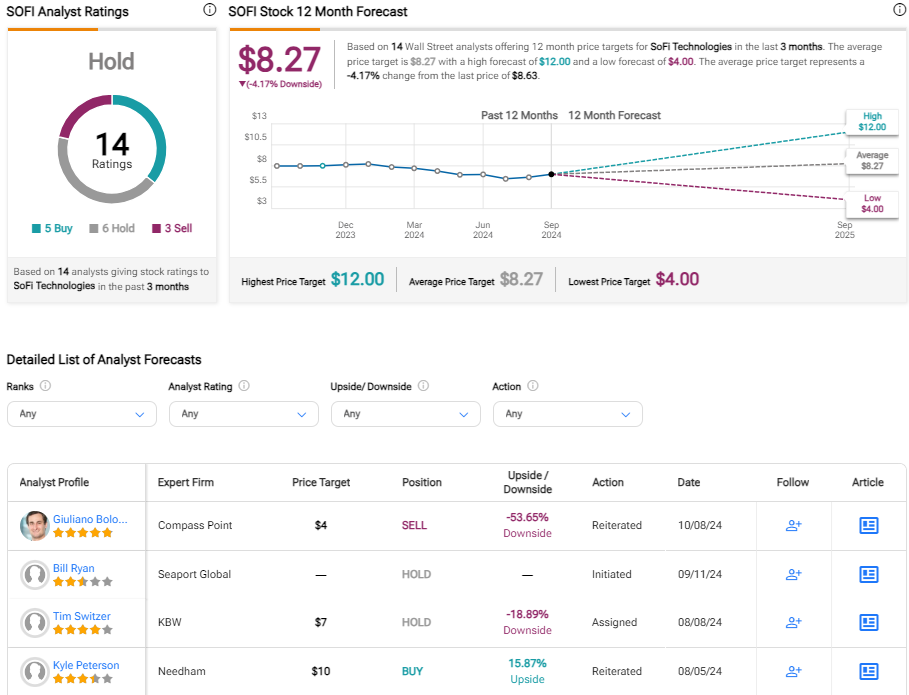

Is SOFI a Buy, According to Wall Street Analysts?

Despite the bullish arguments presented in this article, Wall Street remains cautious about SOFI stock. Of the 14 analysts covering the stock, only five recommend a buy, six rate it a hold, and three suggest a sell, leading to an overall consensus of hold according to TipRanks. The average price target for SOFI stock is $8.27, approximately 5% below the recent market price.

conclusion

In sum, despite short-term challenges and cautious analyst sentiment, SoFi’s strong revenue growth, improving profitability and strategic diversification make a compelling case for growth at a reasonable valuation for long-term investors. With a rapidly expanding member base and a digital-first strategy, I believe the company is well positioned to thrive in the evolving fintech landscape. This ensures bullish sentiment for SOFI stock at current prices.

Disclosure

Disclaimer

Comments are closed, but trackbacks and pingbacks are open.