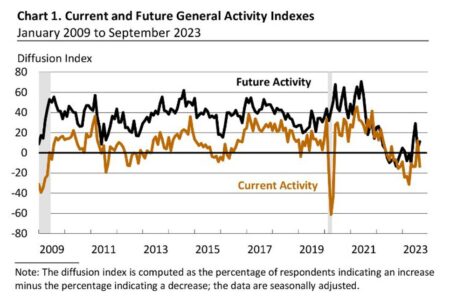

Philadelphia Fed business activity index falls to -12.0

- For the full report CLICK HERE

- Prior month 12.0

- Philly Fed business index -13.5 vs -0.7 estimate. This is the 14th negative reading in the past 16 months

- Capital expenditures six-month forward 7.5 versus -4.5 last month

- Employment -5.7 versus -6.0

- Prices paid 25.7 versus 20.8 last month

- prices received 14.8 versus 14.1 last month

- New orders -10.2 versus 16.0 last month.

- Shipments -3.2 versus 5.7 last month.

- Unfilled orders -13.6 versus -4.8 last month

- delivery times -14.9 versus -7.0 last month.

- Inventories 8.9 versus -10.2 last month.

- Average employee work 4.7 versus 6.3 last month

The six-month forward

- business activity index came in 11.1 versus 3.9 last month

- new orders 25.6 versus 18.2 last month

- employment 6.5 versus 12.0 last month

- shipments 30.5 versus 14.9 last month

- prices paid 48.0 versus 53.0 last month

- prices received 36.5 versus 40.6 last month

- average work week -1.3 versus 8.3 last month

On the surface, the headline number was weaker but things like prices paid remained elevated. The six-month forward business index was also stronger although there was some declines in the prices paid and received indices. New orders however were higher as were shipments expectations.

The detailed summary from the Philadelphia Fed said:

- Manufacturing activity in the region declined in September, reversing positive trends seen in August.

- Key indicators like general activity, new orders, and shipments returned to negative territory.

- General activity index fell from 12.0 in August to -13.5 in September.

- New orders index dropped from 16.0 to -10.2.

- Shipments index declined 9 points to -3.2.

- Employment continued to decline, with the index at -5.7.

- 19% of firms reported a decrease in employment, 14% reported an increase, and 67% reported no change.

- Price indexes remained stable and near long-run averages.

- Prices paid diffusion index rose 5 points to 25.7.

- Current prices received index was little changed at 14.8.

- Production and capacity utilization showed little change.

- Median current capacity utilization rate remained at 70 to 80%.

- Labor supply was reported as a constraint by some firms, but 34% indicated it was not a constraint.

- Supply chains were not a constraint for 46% of firms, up from 27% in June.

- Future outlook:

- Most firms expect impacts of various factors to stay the same.

- 22% expect COVID-19 impacts to worsen, up from 0% in June.

- 24% expect worsening impacts from energy markets.

- Over one-fifth expect the impacts of financial capital to worsen.