Investors initially bought into the hype. Charging point (NYSE: CHPT) And other charging infrastructure companies. This was a logical trend as the electric vehicle industry prepares to boom in the coming years. In fact, some of the biggest concerns facing potential EV customers are range anxiety and charging infrastructure availability, issues that ChargePoint can help solve.

Despite the growth of the electric vehicle market — albeit slower than expected — ChargePoint has struggled to deliver revenue growth to investors. But with its recent shift from growth to profitability, can the company turn its business around and reward investors?

Bad news

A bad sign for the charging infrastructure startup is that while many EV startups are burning through cash as they scale, fewer are reporting revenue declines. ChargePoint’s fiscal first quarter of 2025 saw revenue decline 18%, from $130 million a year earlier to $107 million. Management also lowered its second-quarter revenue guidance from a range of $150 million to $165 million to a range of $108 million to $113 million.

Moreover, the company ended the first quarter of fiscal 2025 with just $262 million in cash and cash equivalents, and has already increased its outstanding shares by more than 30% over the past three years. If it needs to raise more capital, investors could be exposed to further cuts.

With the broader U.S. electric vehicle market slowing, at least temporarily, ChargePoint will continue to struggle for revenue growth in the near term. But management is shifting its strategy to focus on profitability, rather than more expensive growth.

Software vs Hardware

More recently, management has decided to focus on software development, which makes sense because it brings higher margins and recurring revenue. The company has announced several hardware partnerships to help bring products to market faster and at lower cost.

One partnership that will help ChargePoint achieve better results is its agreement to jointly develop electric vehicle charging solutions with AcBel, a leading power supply manufacturer under the Kinpo Group. The agreement will improve ChargePoint’s R&D capabilities, reduce costs, and bring more innovative products and solutions to market faster.

Another partnership that will move investors came with LG ElectronicsThe two companies are targeting commercial charging solutions, with deliveries expected to begin this summer. Essentially, the deal calls for ChargePoint to operate LG’s charging stations using its software, and ChargePoint users to benefit from LG’s high-quality EV chargers as the company currently doesn’t offer hardware solutions.

Is the stock worth buying?

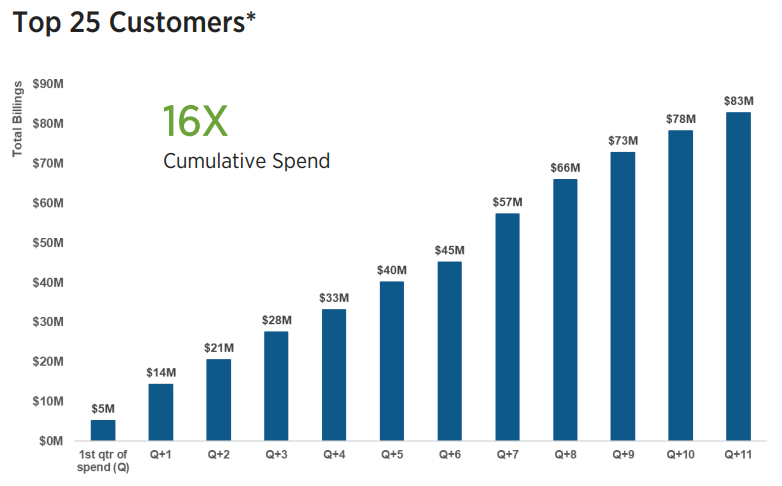

ChargePoint is benefiting from a new focus on software, thanks to its software-as-a-service (SaaS) offerings for its commercial and fleet products. In fact, according to ChargePoint’s investor presentation, the company works with 74% of the Fortune 50 companies, and revenue from its largest customers continues to grow organically.

Finally, with the shift to software and profitability rather than growth, management expects to generate positive adjusted earnings. earnings before interest, taxes, depreciation and amortization In the fourth quarter of fiscal 2025. This would be a big step for the company toward proving to investors that it has a long-term path to returning value to shareholders. For investors willing to accept the risks that come with a cash-burning startup, ChargePoint offers a cheaper entry point — it has lost more than 90% of its value over the past three years — to invest in The electric car market looks set to continue to grow..

Don’t miss this second chance for a potentially lucrative opportunity.

Have you ever felt like you missed out on the most successful stocks? Then you’ll want to hear this.

In rare cases, our team of expert analysts issue Double Down stock Recommendation for companies they think are about to explode. If you’re worried you’ve already missed out on an investment opportunity, now is the best time to buy before it’s too late. The numbers speak for themselves:

-

Amazon: If you invested $1,000 when we doubled it in 2010, You will have $18910.!*

-

apple: If you invested $1,000 when we doubled it in 2008, You will have $41,544.!*

-

Netflix: If you invested $1,000 when we doubled it in 2004, You will have $330,931.!*

Right now, we’re issuing “double-up” alerts for three amazing companies, and there may not be another opportunity like this anytime soon.

See 3 “Double-Bearing” Stocks »

*Stock Advisor returns as of July 29, 2024

Daniel Miller He has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has Disclosure Policy.

ChargePoint is trending toward profitability, but is it a stock worth buying? Originally posted by The Motley Fool

Comments are closed, but trackbacks and pingbacks are open.