A combination of risk-off flows and upbeat U.S. retail sales data lifted the Greenback against its counterparts in the past trading sessions.

Treasury yields were also on the rise while stock indices didn’t seem too cheery about the prospect of borrowing costs staying higher for longer.

Headlines:

- Middle East conflict remained heightened after Iran warned that it will immediately respond to any potential counterattacks from Israel

- Eurozone industrial production for March: 0.8% m/m (0.8% expected, 3.0% previous)

- U.S. headline retail sales for March: 0.7% m/m (0.4% expected, 0.9% previous), core retail sales up 1.1% (0.5% expected, 0.6% previous)

- U.S. Empire State manufacturing index for April: -14.3 (-5.2 expected, -20.9 previous)

- Fed official Williams said that rate cuts are still likely this year if inflation continues to slow

Broad Market Price Action:

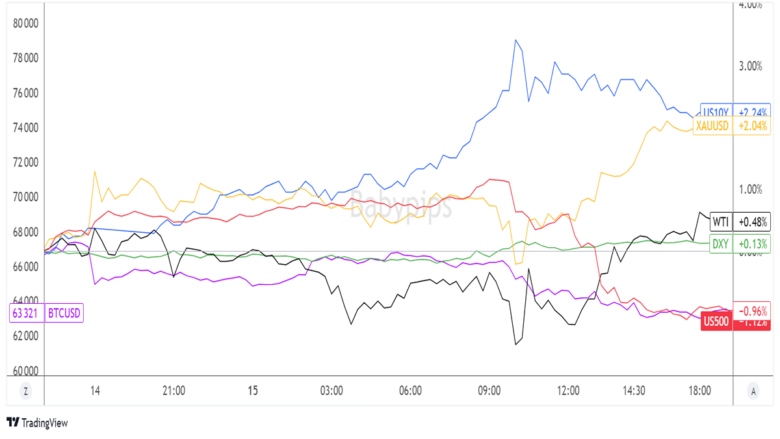

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Risk assets were off to a lackluster start, as traders weighed the potential impact of worsening geopolitical tensions in the Middle East on the financial markets.

Even crude oil dipped, along with other commodities, before bottoming out and pulling higher to positive territory during U.S. trading hours. Gold found support at the previous week lows and resumed its climb back above the $2,350 region.

Treasury yields raked in significant gains when the U.S. retail sales report was printed, as stronger than expected figures once again fueled expectations of a pushback in Fed easing plans. On the flip side, the S&P 500 index turned south on the prospect of higher borrowing costs weighing on business and consumer activity.

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Major Currencies Chart by TradingView

After some sideways price action early in the day, the dollar was once again the king of pips thanks to an upbeat U.S. retail sales report.

The March headline figure showed an impressive 0.7% month-over-month gain, surpassing the consensus of a 0.4% uptick, while the core reading printed a 1.1% increase versus the estimated 0.5% rise.

This allowed the U.S. currency to shrug off the downbeat Empire State manufacturing index for the current month, as traders are likely holding out for the rest of the regional indices due in the next few days.

Upcoming Potential Catalysts on the Economic Calendar:

- U.K. claimant count change at 6:00 am GMT

- German and eurozone ZEW economic sentiment index at 9:00 am GMT

- Canadian CPI figures at 12:30 pm GMT

- U.S. industrial production data at 1:15 pm GMT

- BOE Governor Bailey’s speech at 5:00 pm GMT

- BOC Governor Macklem’s speech at 5:15 pm GMT

- Fed Chairman Powell’s speech at 5:15 pm GMT

- New Zealand quarterly CPI at 10:45 pm GMT

Volatility is likely to stay elevated in the next trading sessions, as the schedule is filled with jobs data and a couple of major CPI releases, not to mention testimonies by THREE central bank heads!

Make sure you check out our Event Guide for Canada’s CPI report if you’re planning on trading this event.

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!

Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!