Markets were having a pretty chill time during the Asian market hours before all hell broke loose in the latter trading sessions.

What’s up with that?!

The dollar even snapped its winning streak and wound up with steep losses against majority of its peers while crude oil and U.S. equities took major hits as well.

Headlines:

- New Zealand Q1 2024 CPI: 0.6% q/q (0.6% expected, 0.5% previous)

- Japanese trade balance for March 2024: -0.70 trillion JPY (-0.30T JPY expected, -0.57T JPY previous); exports up for the fourth month in a row

- Australia’s MI leading index for March 2024: -0.1% (+0.1% previous)

- U.K. headline CPI for March 2024: 3.2% y/y (3.1% expected, 3.4% previous); core CPI at 4.2% y/y (4.1% expected, 4.5% previous)

- U.K. PPI input prices for March 2024: -0.1% m/m (+0.1% expected, +0.3% previous); PPI output prices at 0.2% m/m (0.2% expected, 0.3% previous)

- BOE MPC member Greene says there are encouraging signs on U.K. inflation

- EIA crude oil inventories reflected 2.7M barrel increase (1.6M expected, 5.8M previous)

- BOE Governor Bailey says latest CPI numbers are in line with forecasts, expects next inflation report to show large decline

- ECB head Lagarde reiterates possibility of June rate cut, adds that growth in Europe is mediocre compared to U.S.

- ECB official Nagel suggests that June easing is increasingly likely, as core and services inflation remain elevated

- Fed Beige Book reports slight growth among districts but signaled moderating wage pressures

- Australia’s employment change for March 2024: -6.6K (+7.2K expected, +117.6K previous); unemployment rate up from 3.7% to 3.8%

Broad Market Price Action:

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Mostly rangebound price action during Wednesday’s Asian trading session turned out to be the calm before the storm, as asset classes chalked up steep losses later in the day.

In particular, WTI crude oil staged a sharp decline upon seeing a slightly larger than expected build in EIA inventories, even though the actual gain of 2.7 million barrels was still lower than the earlier 5.8 million barrel increase.

Interestingly enough, there were no other major catalysts tied to the selloff, apart from a fresh batch of central bank commentary and the U.K. CPI release.

Gold also retreated from its highs, rounding up nearly 1% in losses for the day, while the S&P 500 index ended in the red. The dollar and Treasury yields found themselves in negative territory as well, even after Fed officials and the Beige Book pointed to the possibility of delaying interest rate cuts this year.

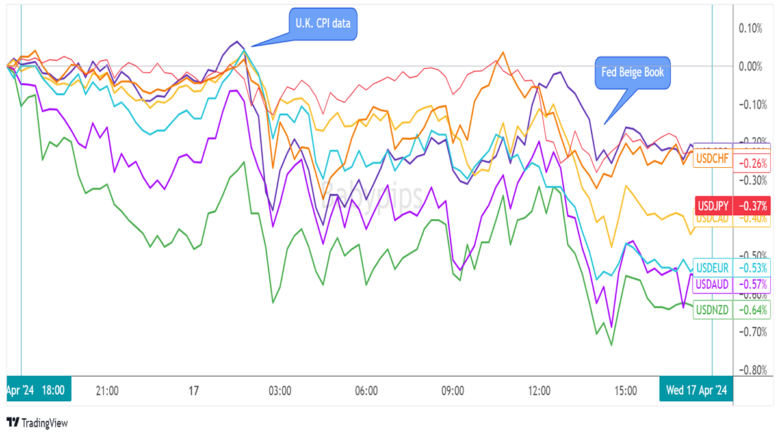

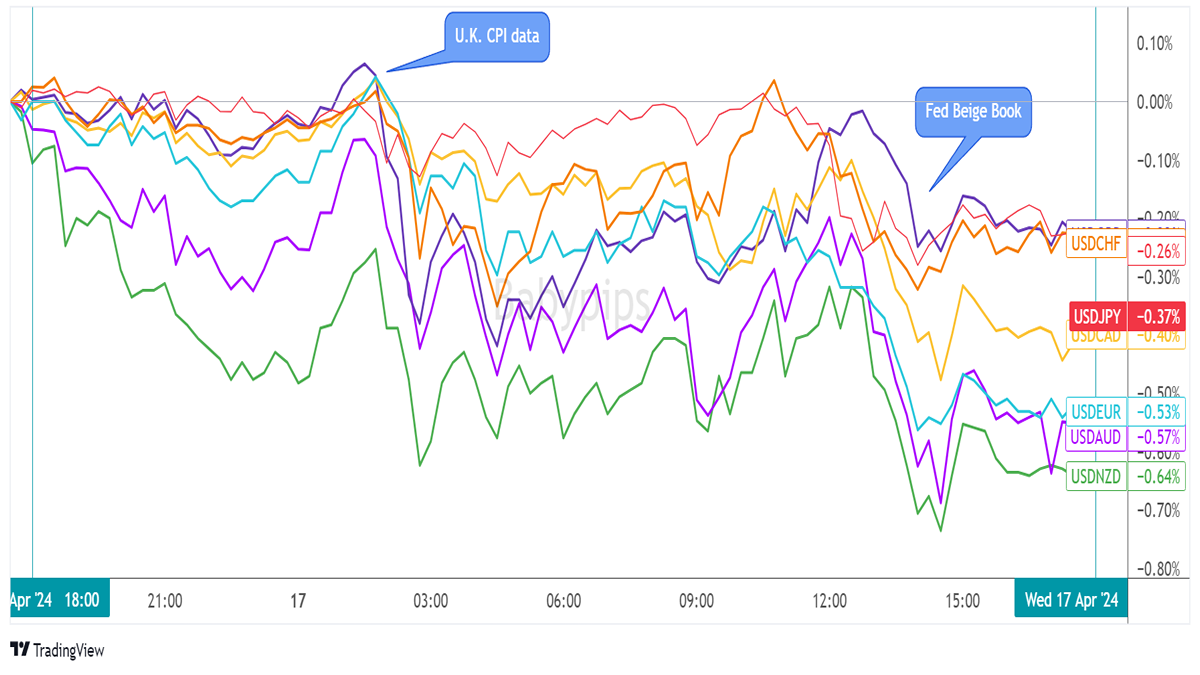

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Major Currencies Chart by TradingView

Dollar price action was choppy for the most part of the day, with the currency barely finding any directional cues from market catalysts.

New Zealand’s latest inflation figures seem to have dampened expectations for RBNZ easing enough to prop the Kiwi up against the U.S. currency early in the Asian session.

The upbeat U.K. CPI release also triggered a pop higher for sterling, as the numbers suggested that the BOE might keep sitting on its hands for much longer, seemingly kickstarting a general wave lower for the dollar across the board as well.

Even the euro managed to rake in gains, despite repeated calls for a June cut by the likes of ECB’s Lagarde, Nagel, and Centeno.

From there, the Greenback resumed its sideways price action before taking another turn lower upon seeing the Fed Beige Book. As it turned out, Fed districts reported difficulties among firms when it comes to passing higher costs to consumers, as spending activity has already been muted.

Upcoming Potential Catalysts on the Economic Calendar:

- Japanese tertiary industry activity index at 4:30 am GMT

- U.S. initial jobless claims at 12:30 pm GMT

- U.S. Philly Fed index at 12:30 pm GMT

- FOMC member Bowman’s speeches at 1:05 am GMT and 1:15 am GMT

- U.S. existing home sales at 2:00 pm GMT

- FOMC member Bostic’s speech at 9:45 pm GMT

- Japanese national core CPI at 11:30 pm GMT

There’s not much in the way of top-tier catalysts in the upcoming trading sessions, although it’s helpful to note that the U.S. initial jobless claims figure tends to generate strong intraday volatility for USD pairs.

With that, make sure you keep close tabs on headlines that cover geopolitical risks and might also influence overall risk sentiment!

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!

Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!