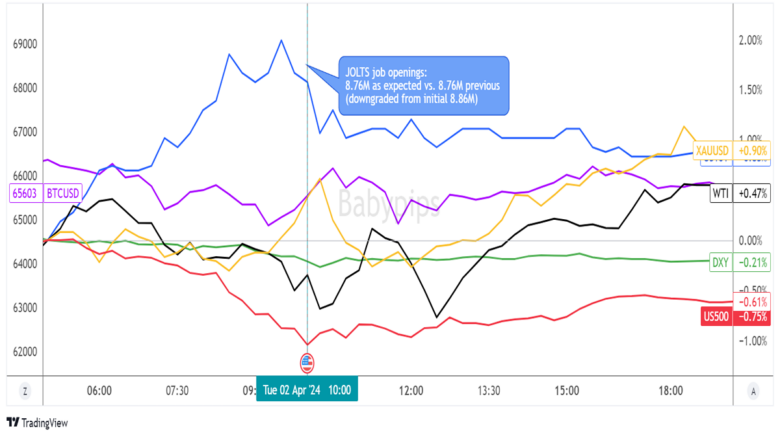

Intermarket price action was as mixed as a bag of nuts in the past session, as Treasury yields stole the show with notable gains, even though the U.S. dollar was on shaky footing.

Meanwhile, gold and crude oil had another positive run while bitcoin and equity indices were in the red.

What is up with all that?!

Headlines:

- Germany Harmonised CPI read for March: 2.3% y/y (2.4% y/y forecast; 2.7% y/y previous)

-

HCOB Eurozone Manufacturing PMI for March: 46.1 vs. 46.5 previous; input & output prices fell

- HCOB Germany Manufacturing PMI for March: 41.9 vs. 42.5

- HCOB France Manufacturing PMI (Final) for March: 46.2 vs. 47.1

- S&P Global U.K. Manufacturing PMI for March (Final) 50.3 vs. 47.5 in February

- Swiss retail trade turnover in February 2024: -0.2% m/m (0.1% m/m forecast; 0.3% m/m previous)

- U.S. JOLTs Job Openings for February 2024: 8.8M (8.84M forecast; 8.75M previous)

- U.S. Factory Orders for February 2024: 1.4% m/m (1.3% m/m forecast; -3.8% m/m previous)

- Global Dairy Price Index change: 2.8% vs. -2.8% previous

Broad Market Price Action:

Treasury yields were on the rise early in the session, despite a lackluster run for the U.S. dollar. The JOLTS job openings figure merely came in line with estimates for February at 8.76 million, but it’s worth noting that the earlier reading was downgraded from 8.86 million to just 8.75 million.

On a more upbeat note, the U.S. factory orders figure came in stronger than expected with a 1.4% month-over-month gain in February versus the estimated 1.1% increase. This was not enough to cheer equity investors on, though, as the S&P 500 index chalked up a 0.7% loss for the day.

Risk assets looked mixed, with bitcoin also chalking up another day in the red while gold and crude oil were in the green.

FX Market Behavior: Majors vs. U.S. Dollar

Overlay of USD vs. Major Currencies Chart by TradingView

The JOLTS job openings report sparked a round of losses for the Greenback across the board, although the losses were muted against the Loonie, as traders turned their focus to the downgraded figure for January.

Even though the February reading came in line with estimates, the negative revision suggested slower momentum when it comes to hiring opportunities and might be hinting at a potential NFP miss.

In addition, FOMC officials merely supported the idea of three interest rate cuts this year instead of downplaying easing expectations, keeping the dollar in a general downward trajectory for the rest of the session, except against the Swiss franc.

Upcoming Potential Catalysts on the Economic Calendar:

- Eurozone flash headline and core CPI estimates at 9:00 am GMT

- U.S. ADP non-farm employment change at 12:15 pm GMT

- FOMC member Bostic’s speech at 12:30 pm GMT

- U.S. ISM services PMI at 2:00 pm GMT

- EIA crude oil inventories at 2:30 pm GMT

- FOMC head Powell’s speech at 4:00 pm GMT

Among the top-tier catalysts lined up in the next trading sessions, the ADP non-farm employment figure and jobs component of the U.S. ISM services PMI might hog the spotlight, as dollar traders are keen on finding NFP clues from leading jobs indicators.

Still, make sure to keep your eyes and ears peeled for Fed remarks coming from FOMC officials, including main main Powell himself, as these could further underscore Fed rate cut bets.

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!

Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!