Strong US economic release has brought back the Fed's “Higher Longer” bets!

What does this mean for major financial assets?

We take a closer look at their reactions:

Titles:

- Inflation in Australia Slowed but still faster than expected in the first quarter of 2024

- Germany IFO Business Climate April: 89.4 (88.9 expected; 87.9 previous)

- API: US crude stocks Unexpectedly decreased by 3.2 million barrels for the week ending April 19 versus an expected increase of 1.8 million and the previous 4.09 million.

- Central Bank of Iraq Industrial trends in the UK Survey for April. Business sentiment rose to +9% from -3% in January. Domestic selling prices rose to +10% from +2% in January

- Environmental impact assessment of commercial crude oil reserves in the United States Decreased by -6.4 million vs. 2.74 million previously

- Retail sales in Canada For February: -0.1% mo/m (0.1% mo/m forecast: -0.3% mo/m previous); Core Retail Sales were -0.3% MoM (expect 0.2% MoM; 0.4% MoM previously)

- American Durable Goods Orders for March: 2.6% m/m (2.2% m/m forecast; 0.7% m/m previously); Baseline reading came in at 0.2% mo/m (expect 0.3% mo/m; previously 0.1% mo/m)

- Takao Ochi, executive director of the Liberal Democratic Party of Japan, is there There is no “broad consensus” on intervention in the yen Now, but a decline of “160 or 170 for the dollar” may prompt “some measures.”

- Member of the Governing Council of the European Central Bank, Joachim Nagel He would prefer a rate cut in June but believes it will be “It does not necessarily have to be followed by a series of interest rate cuts.“

- China's leading economic indicator CB Slight improvement from -0.3% to -0.2% in March; “Lower consumer expectations continue to push LEIs downward.”

Broad market price movement:

Dollar Index, Gold, S&P 500, Oil, 10-Year US Yields, Bitcoin Overlay Chart by TradingView

An extension of relatively risk-friendly trading conditions from the previous day supported demand for several major financial assets early yesterday.

However, the tables turned during the London and US sessions, as positive economic reports out of the US revived concerns about a “higher for longer” interest rate environment.

US 10-year bond yields rose on the Fed's imprudent bets, spot gold capped the day in the red, and the S&P 500 fell despite positive corporate earnings results.

Meanwhile, Bitcoin (BTC/USD) fell sharply after a bearish technical breakout, and US crude oil prices weakened on easing geopolitical and supply concerns (API and EIA reports still show enough supply despite their declines).

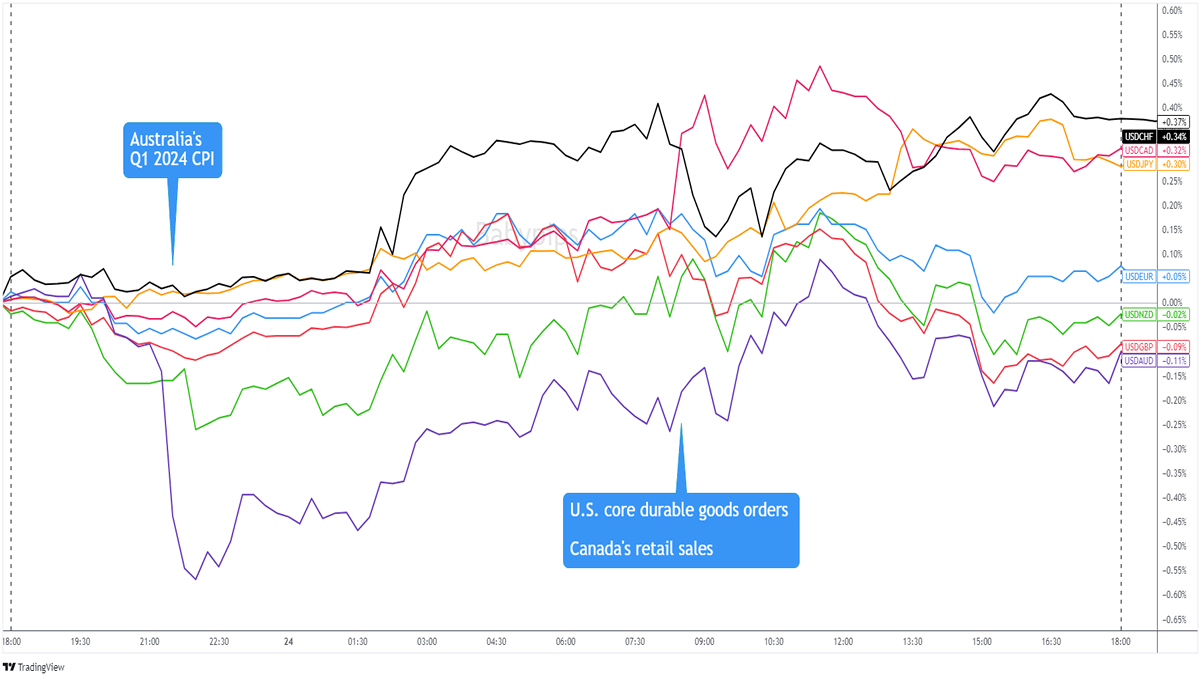

Forex market behavior: US dollar against major currencies

Overlay of the US dollar against major currencies Chart by TradingView

The US dollar started the day in tight ranges except against the Australian dollar and New Zealand dollar which were supported by hotter than expected Australian inflation and stronger export activity in New Zealand.

The US dollar then slowly rose in the late Asian and early European sessions, perhaps due to traders taking profits ahead of the US GDP and core PCE releases. The US dollar also struggled to gain traction against the euro after a strong German confidence report and the pound after strong data from the UK.

Stronger-than-expected US core durable goods orders provided the US dollar with new highs in the US session but a bit of profit taking towards the end of the session pushed the dollar back closer to its open levels in the US session.

The US dollar is still strong against other safe haven currencies such as the Swiss franc and the Japanese yen (USDJPY is now above 155.00!) but is struggling against major currencies such as the Australian dollar and the New Zealand dollar and European currencies such as the euro and British pound.

Potential catalysts coming on the economic calendar:

- Australia and New Zealand markets are out on bank holiday

- GfK German Consumer Climate at 6:00 AM GMT

- ECB Economic Bulletin at 8:00 AM GMT

- US GDP and GDP price index are provided at 12:30 PM GMT

- Initial US unemployment claims at 12:30 PM GMT

- Initial US wholesale inventories at 12:30 PM GMT

- US Home Sales Pending at 2:00 PM GMT

- ECB Governing Council member Joachim Nagel will deliver a speech at 3:15pm GMT

- UK GfK Consumer Confidence Index at 11:01 PM GMT

- Core CPI will be released in Tokyo at 11:30 PM GMT

- Australia's quarterly producer price index at 1:30am GMT (April 26)

- Bank of Japan policy decision during the Asian session (April 26)

We get the first estimates of Uncle Sam's growth for the first quarter of 2024!

Then there's the Bank of Japan, which could say a thing or two (or twenty) about the yen's new weakness.

Will US GDP report lead to a repricing of Fed rate bets? Will the Bank of Japan decide to intervene in currency markets? Stay tuned!

Are you looking for your own place to record your market observations and trading statistics? If so, check out TRADEZELLA! It's easy to use

A blogging tool that can lead to valuable insights about performance and strategy! You can easily add your thoughts, plans and track your psychological state with each trade. Click here to see if this is right for you!Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe using our affiliate links, it helps us maintain and improve our content, much of which is free and available to everyone – including Pipsology School! We appreciate your support and hope you find our content and services useful. Thank you!