The market holiday in Japan and the lack of verbal intervention from Japanese officials weren’t enough to stop the yen from making big moves!

Here’s how it all went down.

Headlines:

- Major city in southwest China (Chengdu) removed home-buying curbs to support property sector

- Germany preliminary CPI for April: 0.5% m/m (0.6% expected, 0.4% previous)

- Spanish flash CPI for April: 3.3% y/y (3.4% expected, 3.2% previous)

- U.K. BRC price shop index for April: 0.8% y/y (1.3% previous)

- Crude oil tumbles on hopes of a political solution being reached in Gaza

- Japan’s “top currency diplomat” Kanda warns that currency movement has bigger impact on import prices now, ready to take action 24 hours a day

- Japanese PM Kishida says he won’t comment on forex intervention despite USD/JPY breaching 160

- Japanese unemployment rate for March: 3.6% (3.5% expected, 3.6% previous)

- Japan’s preliminary industrial production for March: 3.8% m/m (3.4% expected, -0.6% previous)

- Japanese retail sales for March: 1.2% y/y (2.5% expected, 4.7% previous)

- New Zealand ANZ business confidence index for April: 14.9 (22.9 previous)

- Australian retail sales for March: -0.4% m/m (+0.2% expected, +0.2% previous)

- Chinese official manufacturing PMI for April: 50.4 (50.3 expected, 50.8 previous)

- Chinese official non-manufacturing PMI for April: 51.2 (52.3 expected, 53.0 previous)

Broad Market Price Action:

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

News of a major city in China lifting home-buying curbs over the weekend led to a positive start for Asian equities on Monday. Gold and oil pulled higher from Friday’s tumble while U.S. bond yields continued to drop.

However, crude oil returned some of its gains as the day went on thanks to rumors of a possible ceasefire in Gaza prompting investors to book profits off long positions based on global supply risks.

Meanwhile, the dollar index and the S&P 500 cruised generally sideways, as traders are likely holding out for another batch of top-tier U.S. data this week that could shape longer-term Fed policy expectations.

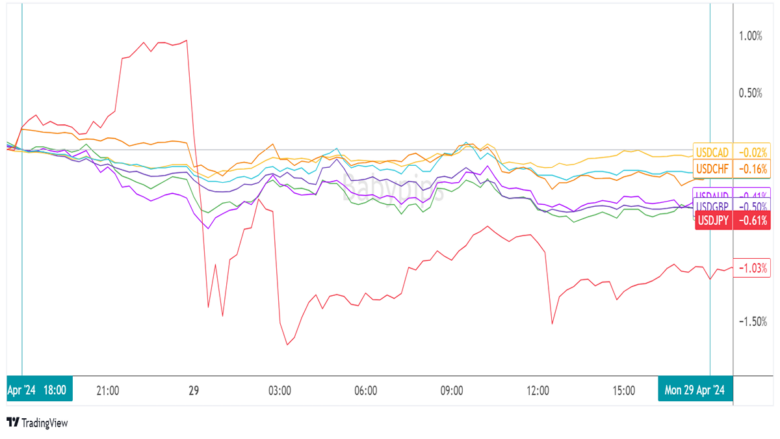

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Major Currencies Chart by TradingView

Liquidity was thin in the FX market during the Asian trading session since Japanese markets were closed for the holiday… but that didn’t stop yen pairs from making huge moves!

USD/JPY popped briefly above the 160.00 handle before dropping like a rock on what seemed to be currency intervention either by the Ministry of Finance (MoF) or the Bank of Japan (BOJ).

Masato Kanda, the country’s top currency diplomat, warned that current yen levels are posing a greater risk to imports at this point and that they are prepared to interfere anytime.

Yen volatility aside, the rest of the major currencies chalked up a few gains against the dollar, as market players may be lightening their USD positions ahead of the FOMC decision. The pound and euro raked in decent pips, despite a mixed performance among European equity indices, while the Loonie was still able to squeeze out small winnings despite the slide in crude oil.

Upcoming Potential Catalysts on the Economic Calendar:

- Chinese Caixin manufacturing PMI at 1:45 pm GMT

- French flash GDP at 5:30 am GMT

- German import prices & retail sales at 6:00 am GMT

- French preliminary CPI at 6:45 am GMT

- Swiss KOF economic barometer t 7:00 am GMT

- Spanish flash GDP at 7:00 am GMT

- Eurozone flash CPI estimates at 9:00 am GMT

- Canada’s monthly GDP at 12:30 am GMT

- U.S. employment cost index at 12:30 am GMT

- U.S. Chicago PMI at 1:45 pm GMT

- U.S. CB consumer confidence index at 2:00 pm GMT

- RBNZ financial stability report at 9:00 pm GMT

- New Zealand quarterly employment change at 10:45 pm GMT

A fresh set of flash CPI and GDP readings are set to shake things up for the euro during the London trading session while New York market traders are likely to focus on the U.S. employment cost index for Q1 2024 and the CB consumer confidence index for April.

From there, the spotlight will probably shift to Kiwi pairs since New Zealand will be printing its quarterly employment change report and labor cost index for the first quarter of the year, likely influencing RBNZ policy bets. Don’t forget to check out our Event Guide for this major market mover!

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use

journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!