Markets started the week on a quiet note as traders remained on the sidelines waiting for potential catalysts this week.

But crude oil was an exception, crude oil prices went up and haven’t looked back!

Find out what market topics moved the markets on Monday:

Headlines:

- Over the weekend, Israel and Lebanon’s Hezbollah reportedly exchanged heavy fire. And risked an all-out war across the Lebanese-Israeli border.

- As expected, People’s Bank of China It kept the one-year fixed-rate mortgage rate at 2.3% and the seven-day reverse repo rate at 1.7% in August.

- Eastern Libyan government It announced the suspension of exports and the closure of all oil fields in eastern Libya.

- German Ifo Business Climate Index It fell from 87.0 to 86.6 in August;German economy increasingly heading towards crisis“

- US Durable Goods Orders Up 9.9% m/m in July; core durable goods down 0.2% (0.0% expected, 0.4% prior)

- China Conference Board Leading Index Improved from -0.3% to 0.0% in July

- BRC UK Shop Price Index It fell 0.3% year-on-year in August after a 0.2% increase in July;Renewed inflationary pressures may be lurking on the horizon.“

- Japan Service Producer Price Index Growth slowed from 3.1% y/y to 2.8% y/y (2.9% expected) in July

Price movement in the broad market:

Dollar Index, Gold, S&P 500, Oil, 10-Year US Treasury Yield, Bitcoin Chart by TradingView

Major assets started the week on a quiet note as investors processed last week’s Jackson Hole insights and remained cautious ahead of this week’s potential market movers.

Volatility spiked during the European session after news emerged that Israel and Hezbollah narrowly avoided an all-out war in southern Lebanon over the weekend. Libya’s shutdown of its eastern oil fields is also likely to push oil prices higher, with WTI jumping from $75.50 to $77.50 before easing back to $77.

In the US, the mixed durable goods report was largely ignored as traders focused on the Federal Reserve’s September rate cut. Still, US stocks had a mixed day: the Dow hit a new record high, while the Nasdaq and S&P 500 fell ahead of Nvidia’s earnings release.

Gold remained near record highs, Bitcoin (BTC/USD) fell to $63,000, and the 10-year US Treasury yield rose from 3.77% to 3.82%.

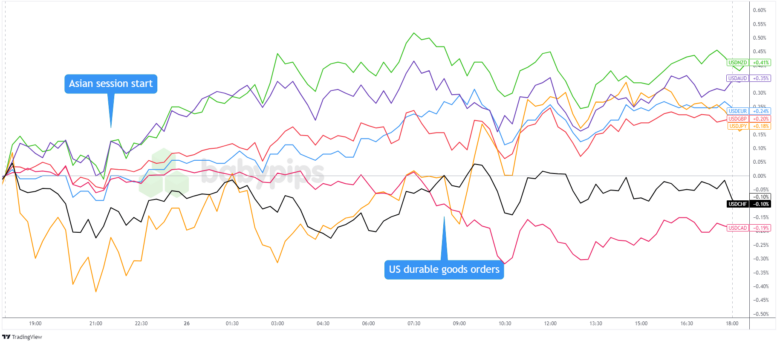

Forex Market Behavior: US Dollar vs Major Currencies:

US Dollar Overlay Against Major Currencies Chart by TradingView

The US dollar started the week on a weak note against other safe havens after JPY’s dovish comments on Friday. The Japanese yen, in particular, saw broad-based gains and fresh intraday highs in early European trading before ending the day with mixed results.

Riskier currencies such as the Australian dollar, New Zealand dollar and British pound saw gains at the start of the US session, but the positive sentiment did not last long as fears of escalating tensions in the Middle East and caution ahead of weekly data releases quickly took hold of markets.

The Canadian dollar performed strongly as it took its cues from higher crude oil prices and ended the day higher across the board.

Potential catalysts coming up on the economic calendar:

- Bank of Japan Core CPI at 5:00 AM GMT

- Germany Final GDP at 6:00 AM GMT

- German GfK Consumer Climate Index at 6:00 am GMT

- UK’s CBI Bank made sales at 10:00 am GMT

- US Home Price Index at 1:00 PM GMT

- US Consumer Confidence Index at 2:00 PM GMT

- Australian CPI at 1:30am GMT (August 28)

Traders may have to take their cues from risk sentiment for another day today as we only have lower-level reports on the docket.

Stay tuned for headlines that could impact geopolitical tensions in the Middle East, as well as potential positions ahead of the most closely watched data releases this week.

Comments are closed, but trackbacks and pingbacks are open.