Major assets were all over the charts on Monday despite the lack of high-level data releases.

Crude oil found support from rising tensions in the Middle East while gold prices fell after hitting new record highs.

How are your other closely monitored assets trading? We have deets!

Titles:

- As expected, The People’s Bank of China lowered key interest rates on 1-year and 5-year loans by 25 basis points in October

- Deputy Governor of the RBA He expressed surprise at the strength of employment growth in Australia and said the labor participation rate was “remarkably high”.

- Producer price index in Germany September: -0.5% monthly (-0.2% expected, 0.2% previously)

- US Conference Board Headline Index for September: -0.5% m/m (-0.3% expected, -0.3% previously)

- Bank of England member Megan Green believes a “cautious and gradual approach” to lowering interest rates is appropriate

- Non-voting Federal Open Market Committee (FOMC) member Lori Logan favors “gradual” interest rate easing amid “significant uncertainties” in the economic outlook.

- Neel Kashkari, a non-voting member of the Federal Open Market Committee, sees “modest cuts over the next few quarters” unless there is “real evidence” of rapid labor market weakness.

- FOMC voting member Jeffrey Schmid It is preferable to “avoid huge moves” and “cut interest rates in a gradual manner” to give time to determine the neutral rate.

- FOMC Voting Member Mary Daly The Fed is expected to continue cutting interest rates as inflation heads toward the 2% target.

- New Zealand’s trade deficit narrowed from NZ$2.3 billion to NZ$2.1 billion in September, as exports (5.2%) exceeded imports (0.9%).

Broad market price movement:

Dollar Index, Gold, S&P 500, Oil, 10-Year US Yields, Bitcoin Overlay Chart by TradingView

The People’s Bank of China (PBOC) started its work on Monday on a positive note by cutting key interest rates on 1-year and 5-year loans as expected. People’s Bank of China (PBOC) Governor Pan Gongsheng also dropped a hint that the bank may lower its reserve requirement ratio (RRR) by 0.2% to 0.5% by the end of the year, while the government outlined new measures to support the technology sector.

However, geopolitical tensions remained. Over the weekend, Israel launched more strikes on Beirut and southern Lebanon, and Hezbollah reportedly fired more missiles at Israel. Stocks also saw some profit-taking, likely driven by rising bond yields and caution ahead of upcoming corporate earnings and economic data.

In the US, the prospect of further gradual easing by the Federal Reserve pushed 10-year Treasury yields higher to 4.20%. Gold, which hit a new record high at $2,740 due to risk-off sentiment and expectations of interest rate cuts, fell to $2,720. Meanwhile, WTI touched $70.30 before falling to $69.80.

US stocks had a mixed close, with the Dow Jones and S&P 500 falling after several record days, while the Nasdaq found support from Nvidia stock rising to a new all-time high. Bitcoin, after being rejected at $69,500, fell on fears of contagion from other risky assets and reached a low of $66,900 before recovering slightly to close around $67,500.

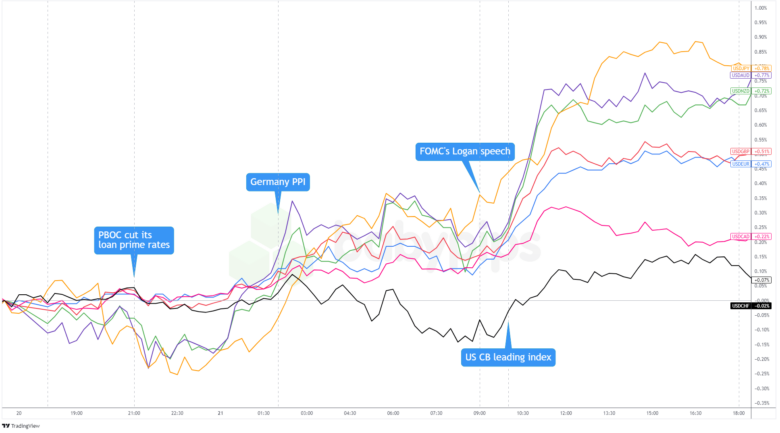

Forex market behavior: US dollar against major currencies:

Overlay of the US dollar against major currencies Chart by TradingView

The US dollar was the king of pips on Monday, thanks to some profit-taking in riskier assets, a bit of risk-off sentiment, and expectations that the Federal Reserve will take its time easing interest rates.

Initially, the US dollar had a mixed start, losing some ground against the yen when the Tokyo Stock Exchange opened and giving up a few points against the Australian and New Zealand dollars after China’s interest rate cut. But by the time Europe opened, the dollar had turned things around, perhaps thanks to rising US bond yields and tensions in the Middle East that sent traders looking for safe havens.

The dollar got another boost at the start of the US session, as stocks saw some profit taking and 10-year bond yields rose. And it didn’t hurt that most Fed officials — both voters and nonvoters — supported the idea of taking things slowly while lowering interest rates.

By the end of the day, the dollar ended trading stronger across the board, with the largest gains against the Australian, New Zealand, and yen. USD/CHF and USD/CAD did not move as much, but ended higher.

Potential catalysts coming on the economic calendar:

- The BRICS summit continues

- UK Public Borrowing at 6:00 AM GMT

- Bank of England Governor Bailey will deliver a speech at 1:25pm GMT

- Bank of England’s Green will speak at 1:45 pm GMT

- FOMC Member Harker will deliver a speech at 2:00 PM GMT

- US Richmond Manufacturing Index at 2:00 PM GMT

- ECB President Lagarde will deliver a speech at 7:15pm GMT

- BoE Member Breeden will deliver a speech at 7:15pm GMT

With not many high-level economic reports, central bankers are likely to take center stage again today. Keep your eyes peeled for speeches by Bank of England Governor Bailey and ECB President Honcho Lagarde, as well as a showcase of speeches by several Bank of England members for clues on the pace of easing in the European region.

Meanwhile, headlines from the BRICS summit could influence overall market risk sentiment. Make sure you stick to the tube if you are trading risk assets this week!

Don’t forget to check out our brand new Forex Correlation Calculator!

Comments are closed, but trackbacks and pingbacks are open.