(Bloomberg) — Chinese companies may be tempted to sell a $1 trillion pile of dollar-denominated assets as the U.S. cuts interest rates, a move that could boost the yuan by as much as 10%, according to Stephen Jin.

Most Read from Bloomberg

The currency is now the biggest risk that is not being priced correctly across all markets – and the yuan could play a big role, said the CEO of Eurozone SLJ Capital.

“Imagine an avalanche,” Jin said of the impact of repatriation flows. “The yuan will appreciate and it may be allowed to do so — it would be modest and acceptable for China to see the yuan appreciate by five to 10 percent.”

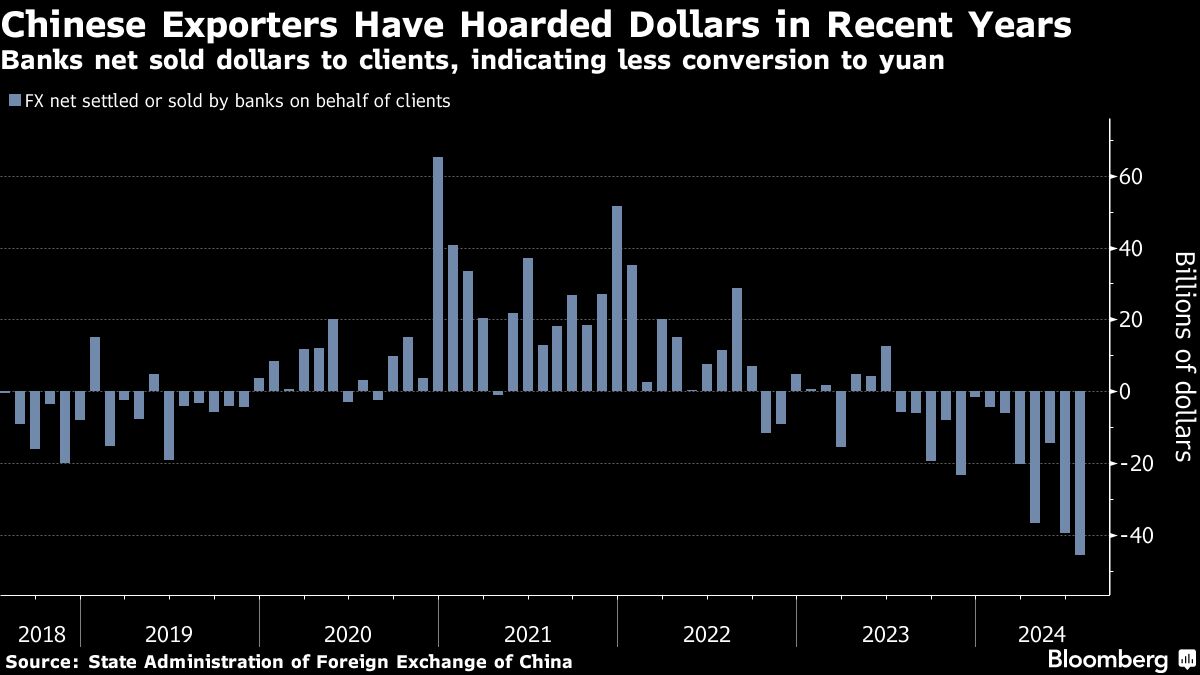

The theory goes like this: Chinese companies may have raised more than $2 trillion in overseas investments since the pandemic, stashed in assets that pay higher interest rates than yuan-denominated ones, according to Jin. When the Fed lowers borrowing costs, the appeal of dollar assets will erode and could spur $1 trillion in “conservative” inflows as the interest-rate discount between China and the U.S. narrows.

Jain, known for his work on the “dollar smile” theory, expects the Fed to cut interest rates more aggressively than markets anticipate if U.S. interest rates continue to fall. That, combined with a strong U.S. dollar, a double-digit U.S. budget deficit, and the prospect of a slow decline, reinforces his belief that the dollar will weaken.

The end result is a Chinese currency that could strengthen against the dollar. It was trading at around 7.12 yuan per dollar on the local market on Monday, after weakening to around 7.28 yuan per dollar in July.

The rally could be even bigger if the People’s Bank of China refrains from intervening to soak up dollar liquidity, London-based Jin said in an interview last week.

The case for a stronger yuan now looks stronger after Federal Reserve Chairman Jerome Powell said at the Jackson Hole symposium on Friday that it was time for the United States to cut interest rates.

But such a move is unlikely to happen immediately after the Fed’s first cut. It could happen when the dollar’s decline accelerates in a so-called soft-landing scenario, or when U.S. inflation eases without triggering a recession, he said.

yuan pressure

Jin’s view is in line with that of Guan Tao, a senior economist at Bank of China International Ltd., who argued that the yuan faces the risk of appreciation if a scenario similar to the yen carry trade collapse occurs.

The ripple effects of the yen’s devaluation have been so severe that they have affected everything from stocks to credit to emerging currencies. A collapse of the yuan-funded carry trade — in which traders borrow the currency cheaply and sell it for higher-yielding alternatives — could unleash fresh waves of panic, especially in Asian markets.

However, Jin said the People’s Bank of China is capable of handling extreme volatility. Beijing has always been wary of aggressive gains in the yuan, as they could hurt export competitiveness and undermine an already slow economic recovery.

China’s foreign exchange regulator is already preparing to assess the impact of a stronger yuan on exporters, people familiar with the matter said. Some strategists have argued that a carry trade focused on a weaker yuan still makes sense given China’s mixed economic fundamentals.

The People’s Bank of China also takes a number of measures to guide market expectations. Recently, the bank has used tools to encourage currency stability, such as its daily reference rate for the yuan onshore and adjustments to the amount of foreign-currency deposits that banks must hold as reserves.

In addition, given that the gap between Chinese and US yields continues to widen despite some gradual contraction recently, companies may not be selling their foreign exchange holdings anytime soon.

Others estimate that the amount of cash available to Chinese companies is somewhat less than Jin’s estimates.

Macquarie Group Ltd. estimates that Chinese exporters and multinationals have amassed more than $500 billion in dollar holdings since 2022. Australia and New Zealand Banking Group Ltd. puts the figure at $430 billion.

“The pressure will be on” for the yuan to rise, Jin said. “Assuming that half of that amount is ‘unrestricted’ money that can be easily triggered by changing market conditions and policies, we are talking about $1 trillion of fast money that could be involved in such a potential run.”

–With help from Qizi Sun.

Most Read from Bloomberg Businessweek

©2024 Bloomberg LP

Comments are closed, but trackbacks and pingbacks are open.