(Bloomberg) — Gold and crude oil fell with Treasuries while US equity futures rose as fears softened over the weekend that the conflict in the Middle East would escalate. Asian stocks fell for a fourth day, with China one of the worst hit as investor sentiment remains fragile.

Most Read from Bloomberg

Oil slipped below $87 a barrel, while gold fell from a five-month high to around $1,970 an ounce as Israel held off on its ground offensive into Gaza amid efforts to secure the release of more hostages. US futures contracts advanced in Asia after the S&P 500 slid more than 1% Friday. Treasuries fell, paring Friday’s rally. The yen briefly weakened past 150 to the dollar.

Markets are starting to wind back some of last week’s haven bid after Hamas released two US hostages and aid started to trickle through Egypt’s border with Gaza at the weekend. Still, Israel has stepped up air raids on Gaza in preparation for the “next phase” of its conflict with Hamas, while also warning that Hezbollah risks dragging Lebanon into a wider regional war.

It’s “a carbon copy of last Monday’s session as we see a partial unwind of the safe-haven flows put on ahead of the weekend,” said Tony Sycamore, an analyst at IG Australia in Sydney.

Chinese stocks dragged the broader Asia equity market further in the red. Property sector woes persisted and confidence took a beating after Beijing launched a series of investigations into Foxconn Technology Group, Apple Inc.’s most important partner and one of the largest employers in country. MSCI’s Asian equity index lost 0.6%, with the Shanghai Composite falling 0.8%.

Elsewhere, the yen briefly weakened beyond 150 per dollar early Monday, a closely watched level for possible intervention by Japanese authorities to support the currency. Bank of Japan officials are pondering whether to tweak their yield-curve control setting at a policy meeting next week, the Nikkei newspaper reported Sunday, without saying where it obtained the information.

“Markets are again on high alert for a possible BOJ intervention,” Commonwealth Bank of Australia strategists including Joseph Capurso wrote in a note to clients. The yen is likely to remain under pressure this week “as the rise in the 10-year Japanese government bond yield, amid growing speculation of BOJ policy tightening, will do little to reduce Japan’s wide bond yield gap with the US,” they said.

Read more: Israel’s Support for Hostage Talks May Delay Invasion of Gaza

Global markets have been whipped around in recent weeks by climbing Treasury yields and growing concern about interest rates staying elevated for longer. Federal Reserve Bank of Cleveland President Loretta Mester said the US central bank is close to wrapping up its tightening campaign if the economy evolves as expected.

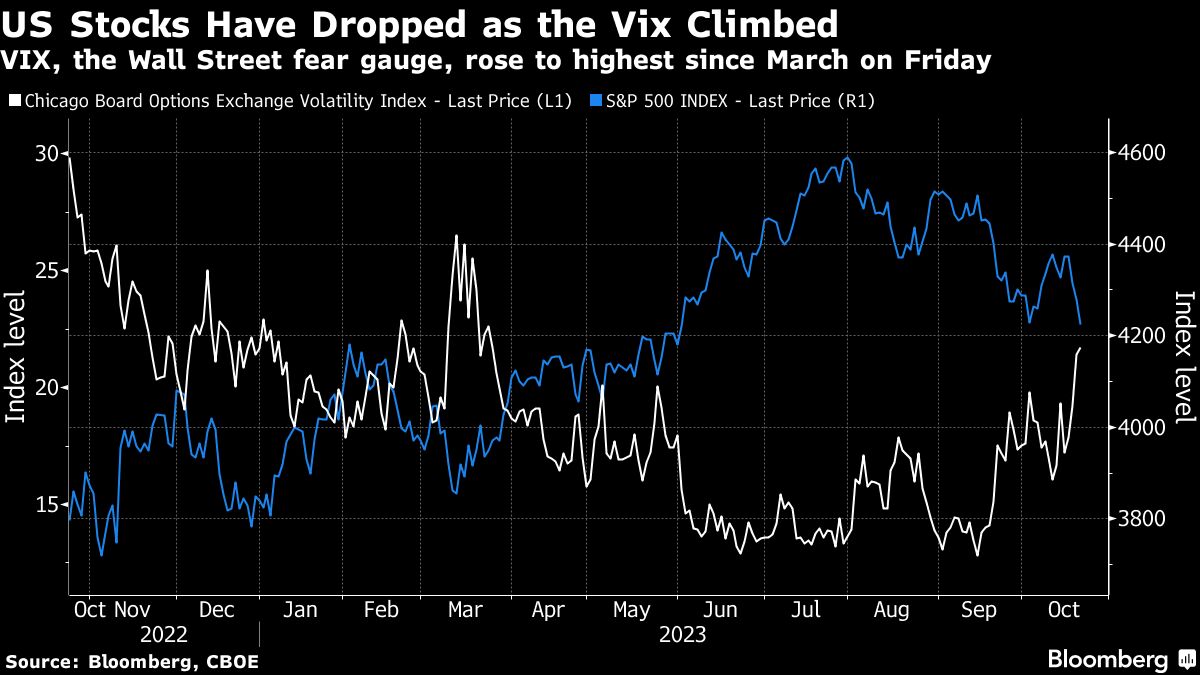

The S&P 500 on Friday slid below its 200-day moving average — seen by some as a bearish signal — and the Cboe Volatility Index, known as the VIX or Wall Street’s “fear gauge,” jumped to its highest since March.

Read more: Record Treasury Bets Build as Traders Split on Fed Rate Outlook

This week, traders will be parsing for clues on the outlook for global interest rates with inflation readings in Australia and Japan as well as economic activity data in the US and Europe. Fed Chairman Jerome Powell is due to give remarks and the European Central Bank will deliver a policy decision later in the week.

Key events this week:

-

Singapore CPI, Monday

-

Taiwan jobless rate, industrial production, Monday

-

Eurozone consumer confidence, Monday

-

EU foreign ministers meet in Luxembourg, Monday

-

Japanese Prime Minister Fumio Kishida delivers policy speech at Diet session, Monday

-

Reserve Bank of Australia Governor Michele Bullock speaks in Sydney, Tuesday

-

Eurozone S&P Global Services PMI, S&P Global Manufacturing PMI, Tuesday

-

UK S&P Global / CIPS Manufacturing PMI, jobless claims, unemployment, Tuesday

-

US S&P Global Manufacturing PMI, Tuesday

-

UN Security Council is expected to open debate on the Middle East, Tuesday

-

Microsoft, Alphabet earnings, Tuesday

-

Australia 3Q CPI, Wednesday

-

Hong Kong Chief Executive John Lee delivers his second policy address, Wednesday

-

Canada rate decision, Wednesday

-

Germany IFO business climate, Wednesday

-

IBM, Meta earnings, Wednesday

-

South Korea GDP, Thursday

-

Turkey rate decision, Thursday

-

European Central Bank rate decision, Thursday

-

EU leaders summit in Brussels, Thursday-Friday

-

Chile rate decision, Thursday

-

US wholesale inventories, GDP, US durable goods, initial jobless claims, Thursday

-

Intel, Amazon earnings, Thursday

-

Japan Tokyo CPI, Friday

-

China industrial profits, Friday

-

Singapore home prices, Friday

-

Spain GDP, Friday

-

US personal spending and income, University of Michigan consumer sentiment, Friday

-

Exxon Mobil earnings, Friday

Some of the main moves in markets:

Stocks

-

S&P 500 futures rose 0.2% as of 1:32 p.m. Tokyo time. S&P 500 Index fell 1.3% on Friday

-

Nasdaq 100 futures rose 0.2%. The Nasdaq 100 fell 1.5%

-

Japan’s Topix fell 0.6%

-

Australia’s S&P/ASX 200 fell 0.9%

-

The Shanghai Composite fell 0.8%

Currencies

-

The Bloomberg Dollar Spot Index was little changed

-

The euro fell 0.2% to $1.0576

-

The Japanese yen was little changed at 149.94 per dollar

-

The offshore yuan was little changed at 7.3272 per dollar

-

The Australian dollar was little changed at $0.6310

Cryptocurrencies

-

Bitcoin rose 2.6% to $30,634.22

-

Ether rose 3.1% to $1,692.35

Bonds

-

The yield on 10-year Treasuries advanced six basis points to 4.98%

-

Japan’s 10-year yield advanced two basis points to 0.855%

-

Australia’s 10-year yield advanced five basis points to 4.79%

Commodities

-

West Texas Intermediate crude fell 1.1% to $87.10 a barrel

-

Spot gold fell 0.4% to $1,973.46 an ounce

This story was produced with the assistance of Bloomberg Automation.

Most Read from Bloomberg Businessweek

©2023 Bloomberg L.P.