- Final Services PMI 52.4 versus 52.8 expected and 53.7 previous.

- Final Composite PMI 52.6 vs. 52.9 expected and 53.8 previous.

Key findings:

- Business activity growth fell to a three-month low in September.

- Strong order books support a positive business outlook for next year.

- Inflation rates slow for the third month in a row.

comment:

Tim Moore, director of economics at S&P Global Market Intelligence, said:

“September PMI surveys suggest that the UK economy remains on a positive path, with improving order books accompanied by an easing of inflationary pressures. More encouraging is the price-driven inflation in the services sector, which acts as a measure of inflationary pressures.” Locally, it fell to its lowest levels since February 2021.

UK providers indicated a moderate expansion in activity in September, driven by resilient business and consumer spending. However, the post-election recovery lost some momentum as output, new work and employment increased at the slowest pace in three months.

Strong domestic demand was recorded throughout the third quarter of 2024, helping to offset headwinds from weak export sales. Survey respondents linked the rise in total new business to renewed growth in the UK economy and the impact of domestic political stability on investment spending.

Some service sector companies commented on delayed decision-making among clients due to business uncertainty ahead of the Autumn Budget on 30 October. However, the majority of survey respondents (56%) expect an increase in business activity over the next year, while only 11% expect a decline.

The resulting index indicated a slight improvement in overall business optimism since August. Lower borrowing costs, easing price pressures and greater certainty about monetary policy expectations helped boost growth expectations in the services sector.

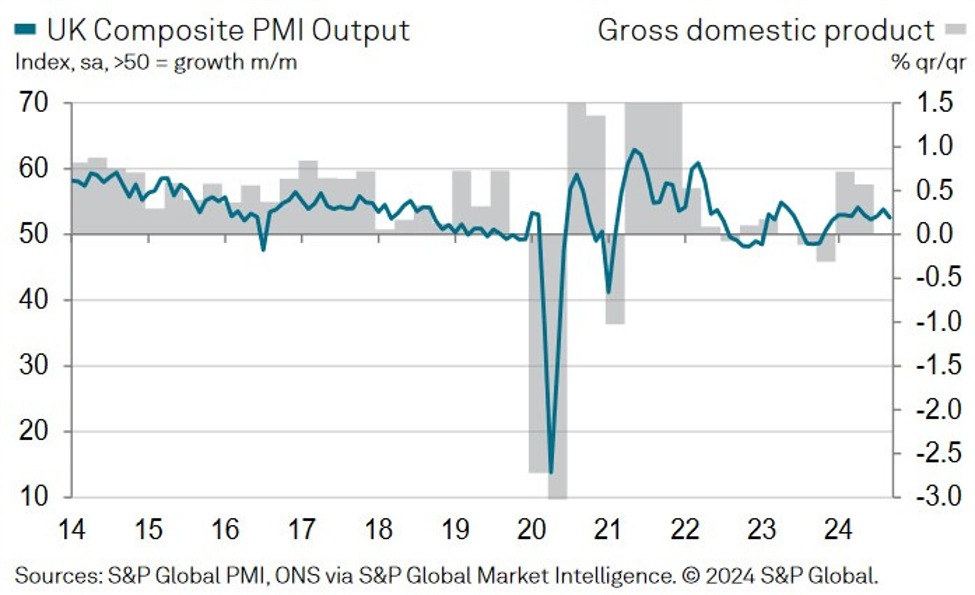

UK Composite PMI

Comments are closed, but trackbacks and pingbacks are open.