(Bloomberg) — The latest sign of underlying price pressures in the United States will offer little hope of settling the debate among Federal Reserve officials over whether they have made enough progress on inflation to let go of the monetary policy brakes.

Most Read from Bloomberg

The Fed’s preferred rate measure on Friday is expected to show that inflation remained high in April, more than double the central bank’s target. The minutes of its early May meeting on Wednesday may help shed some light on officials’ willingness to stand by next month.

Several Fed officials have indicated this week that they are looking to open up as they assess economic data as well as stress in the banking sector. Dallas Fed President Lori Logan said she’s not yet convinced officials should skip a rate hike next month, while Gov. Philip Jefferson said patience is in order.

Read more: Powell steers the policy debate with a clear signal on the June rate pause

The core PCE price index, which excludes the mostly volatile food and energy components, is expected to have increased 4.6% year-on-year, matching the previous month’s annual rise. On a monthly basis, the core gauge is expected to rise 0.3% for the second month.

The Personal Income and Spending report is also expected to show that inflation-adjusted consumer expenditures remained flat at the start of the second quarter. This helps explain why economists expect the US economy to cool down further after expanding at a rate of 1.1% in the first quarter.

What Bloomberg Economics says:

“The Fed’s preferred inflation measure will show little or no progress on inflation over the past month, and the final May reading of the University of Michigan’s Long-Term Inflation Expectations will confirm whether or not the higher initial reading was a fluke.”

—Anna Wong, Stuart Ball, Eliza Winger, and Jonathan Church. For the full analysis, click here

Other US data this coming week includes New Home Sales and Durable Goods Orders for April, as well as revised GDP data for the first quarter.

St. Louis Federal Reserve Chairman James Bullard and Mary Daley of San Francisco are scheduled to speak Monday, while Raphael Bostick of Atlanta and Thomas Parkin of Richmond will discuss disruptive technology at a conference.

Meanwhile, the standoff over the US debt limit is approaching a critical deadline, with June 1 the expected last day that the US can pay its bills in full.

Further north, Canadian jobs data will reveal a detailed picture of earnings, employment and hours worked in March, as some fear rising wages will stand in the way of efforts to slow inflation.

Elsewhere, German data will reveal whether the country succumbed to recession in the first quarter after all, while UK inflation may have slowed significantly. Among multiple interest rate decisions, New Zealand may raise again.

Click here for what happened last week and below is our summary of what is going to happen in the global economy.

Asia

The G7 summit in Hiroshima concludes on Sunday with economic security including diversification of supply chains among the main issues on the agenda.

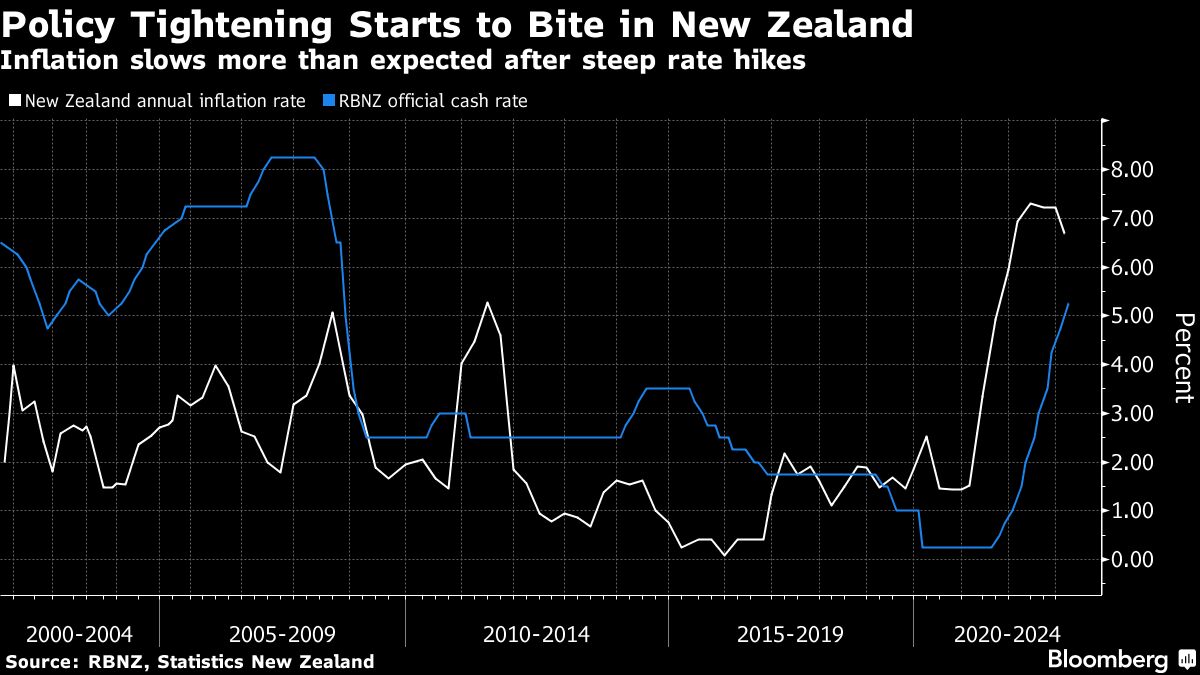

The central bankers of New Zealand, South Korea and Indonesia will make their final decisions on interest rates during the week as a global bout of inflationary tightening draws to a close.

The RBNZ is expected to make at least one increase of 25 basis points after five percentage point increases since late 2021.

Both Bank of Korea and Bank Indonesia have already been suspended since early in the year and they are expected to be fine again.

Chinese banks are likely to keep their benchmark lending rates unchanged on Monday, but pressure is mounting on the central bank to ease policy as the recovery weakens.

Policymakers in Singapore and Malaysia will also be watching the latest price data to check the pace of inflation slowing in their economies.

CPI numbers out of Tokyo on Friday will indicate the national trend in Japan. The deputy prime ministers of Singapore, Vietnam and Thailand will speak, along with the leaders of Sri Lanka and Laos, at a media event in Tokyo this weekend.

Europe, Middle East and Africa

The health of the German economy will take center stage this week with several reports that may indicate continued malaise.

Among them, purchasing managers’ indices for the euro area and its largest member will be released on Tuesday. The IFO survey of German business confidence will be published on Wednesday, with all major measures by economists expected to decline.

On Thursday, a new German GDP estimate will be released. Given the weakness in recent data, economists will be watching for a possible downward revision that could mean a contraction in the first quarter. Such an outcome could mean that the economic slump that many thought the country had been spared has happened after all.

Several ECB officials will be speaking this week including President Christine Lagarde as they celebrate the institution’s 25th anniversary in 1999.

Meanwhile in the UK, economists expect a significant drop in inflation, although with the median forecast at 8.2%, the outcome is likely to underscore the challenge the BoE still faces.

Elsewhere, several central bank decisions are scheduled across the region in the coming week:

-

On Monday, the Bank of Israel is expected to raise interest rates for the tenth time in a row on Monday in an effort to curb stubbornly high inflation.

-

Also on Monday, officials in Ghana are likely to leave the benchmark unchanged as inflation is expected to continue to slow.

-

A day later, the Hungarian central bank may start lowering the highest key rate in the European Union.

-

On Wednesday, Nigeria’s central bank is expected to extend its longest phase of monetary tightening in more than a decade.

-

Also on that day, an Icelandic decision would likely lead to another rally.

-

Turkey is likely to keep interest rates at 8.5% on Thursday, halting a bullish cycle ahead of the second round of presidential elections this month as President Recep Tayyip Erdogan seeks to extend his two-decade rule.

-

On the same day, South African policymakers are widely expected to raise the key interest rate by 50 basis points, on the back of significant rand weakness and steady inflation in an economy courting recession.

-

On Friday, the price of Eswatini, whose currency is pegged to the South African rand, is likely to rise.

latin america

In a very light week in the region, market outlook surveys from Brazil and Mexico will be released for Monday along with weekly trade data in Brazil.

In Peru, the first-quarter production report is expected to show that the economy is weaker than in the previous three months as well as from the same period in the previous year, as high inflation, tough financial conditions and political turmoil take a heavy toll.

A mid-month reading of Brazil’s benchmark inflation indicator could see the annual reading come in at around 4%, well within the central bank’s target range and sensationally close to the 3.25% target.

Paraguay’s central bank is likely to keep its key rate at 8.5% even though inflation is only 5.3% now and appears to be on its way back to the 4% target.

Mexico releases March GDP proxy data and the final reading of first-quarter output, which should highlight the resilience of Latin America’s second-largest economy. Inflation readings in the middle of the month are likely to show further deceleration to bring the annual reading not far from 6% even with the core reading up more than a percentage point.

— With assistance from Jeremy Diamond, Andrea Dudek, Robert Jameson, and Sylvia Westall.

Most Read from Bloomberg Businessweek

© 2023 Bloomberg LP