(Bloomberg) — The Australian dollar and US stock futures rose in early Asian trade on Monday amid signs of improving relations between the United States and China, while index contracts in Asia showed muted moves.

Most Read from Bloomberg

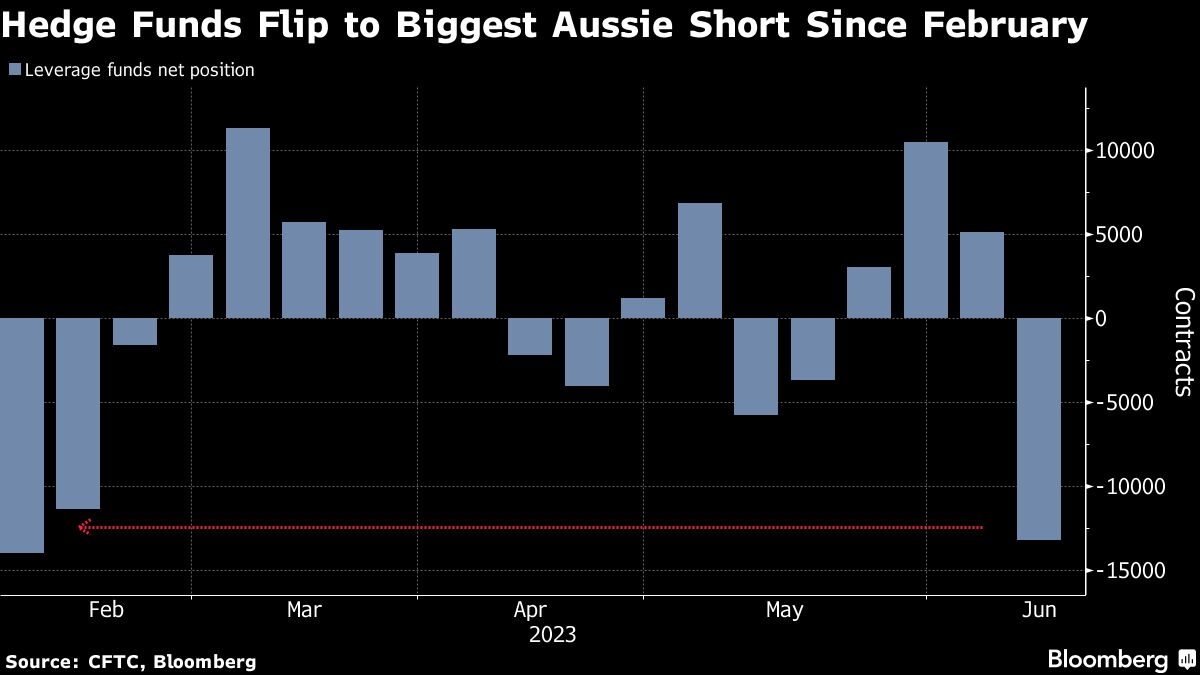

The Australian dollar rose against the greenback, adding to its 2% rally last week – the currency’s third consecutive weekly gain against the greenback. The advance attracted hedge funds to sell the currency.

Monday’s slight advance follows positive signs that Sino-US relations will thaw, as well as continued optimism that China will unleash new stimulus to bolster its flagging recovery.

US Secretary of State Antony Blinken held “frank” talks with his counterpart in Beijing in a meeting that lasted longer than planned. President Joe Biden said Saturday that he hopes to meet Chinese President Xi Jinping in the next few months.

Australian and Hong Kong stock futures fell slightly, reflecting the decline in US stocks on Friday, while Japanese contracts made a small advance.

Investors are closely watching signs of more official support for the Chinese economy after the country cut its main lending rate last week. The country is set to cut key interest rates for one-year and five-year loans in decisions expected on Tuesday, according to economists’ forecasts.

Nomura Holdings, Standard Chartered and Morgan Stanley said authorities may increase the share of local government special-purpose bonds to fund infrastructure investments in a potential stimulus package to boost growth.

“The market’s expectation of policy stimulus is building,” said Kinger Lau, chief China equity strategist at Goldman Sachs. He sees more official support for the economy among a series of drivers that could push Chinese stocks higher. “A number of these supportive catalysts are in place, creating an attractive tactical market for equity operators to take risks,” he said in a note on Monday.

Australian bond yields fell by about 1 basis point while New Zealand yields rose by the same amount after treasury yields rose on Friday. The dollar index was little changed while the yen fell to its lowest level since November on a daily basis.

US stock and bond markets will be closed for the June holiday on Monday. The S&P 500 fell 0.4% on Friday, ending a six-session streak of advances as investors look for more insight into the Fed’s interest rate decisions.

Federal Reserve Chairman Jerome Powell will present his semi-annual report to Congress on Wednesday. St. Louis Federal Reserve Bank President James Bullard is scheduled to speak to his counterparts in New York and Chicago next week.

The Fed kept interest rates unchanged last week but warned of further tightening ahead. In the past, a three-month pause in rate hikes after a series of such rate hikes boosted stock prices.

“We may just have a chance to avoid a recession,” Lauren Gilbert, CEO of Wealthwise Financial, said in an interview with Bloomberg Television. “Markets are already anticipating another rate hike, and our baseline is that may not happen.”

Other key developments for the central bank next week include policy meetings in Turkey, the UK and Switzerland.

Main events this week:

-

June US holiday, Monday

-

China loan initial interest rates, tuesday

-

Residences begin in the US, Tuesday

-

Louis Federal Reserve Bank of St. Louis President James Bullard speaks, Tuesday

-

New York Federal Reserve Bank President John Williams speaks on Tuesday

-

Federal Reserve Chairman Jerome Powell delivers semi-annual congressional testimony before the House Financial Services Committee, Wednesday

-

Chicago Federal Reserve President Austin Goolsby speaks Wednesday

-

Eurozone Consumer Confidence, Thursday

-

Price decisions in the UK, Switzerland, Indonesia, Norway, Mexico, the Philippines and Turkey on Thursday

-

The leading indicator of the US Congressional Council, Initial Jobless Claims, Current Account, Existing Home Sales, Thursday

-

Federal Reserve Chairman Jerome Powell delivers semi-annual congressional testimony before the Senate Banking Committee, Thursday

-

Cleveland Federal Reserve’s Loretta Mester speaks Thursday

-

Eurozone S&P Global Eurozone Manufacturing PMI, S&P Global Eurozone Services PMI, Friday

-

Japanese CPI, Friday

-

S&P Global / CIPS UK Manufacturing PMI, Friday

-

Standard & Poor’s Global Manufacturing Index in the US, Friday

-

Louis Federal Reserve Bank of St. Louis President James Bullard speaks on Friday

Some of the major movements in the markets:

Stores

-

S&P 500 futures were up 0.1% as of 8:20 a.m. Tokyo time. The S&P 500 fell 0.4% on Friday

-

Nasdaq 100 futures rose 0.3%. The Nasdaq 100 fell 0.7% on Friday

-

Nikkei 225 futures rose 0.1%

-

Hang Seng Index futures fell 0.7%.

-

S&P/ASX 200 futures changed little

currencies

-

The Bloomberg Spot Dollar Index has not changed

-

The euro was little changed at $1.0942

-

The Japanese yen was little changed at 141.93 per dollar

-

The external yuan was little changed at 7.1308 per dollar

-

The Australian dollar was not changed much at $0.6878

Digital currencies

-

Bitcoin fell 0.3 percent to $26,395.21

-

Ether fell 0.6% to $1,720.01

bonds

goods

This story was produced with help from Bloomberg Automation.

Most Read by Bloomberg Businessweek

© 2023 Bloomberg LP