The corporate bond market seems to be abruptly cavorting on the risk of a downturn now.

Article content

(Bloomberg) — The corporate bond market appears to be abruptly cacophonous about the risks of an economic downturn now.

Advertising 2

Article content

Job growth is slowing in the US and consumer spending is looking increasingly sluggish. Citigroup analysts including Daniel Soried wrote this week that while US blue chips remain broadly healthy, some early signs of trouble are emerging, including rising costs and pressure on profit margins.

Article content

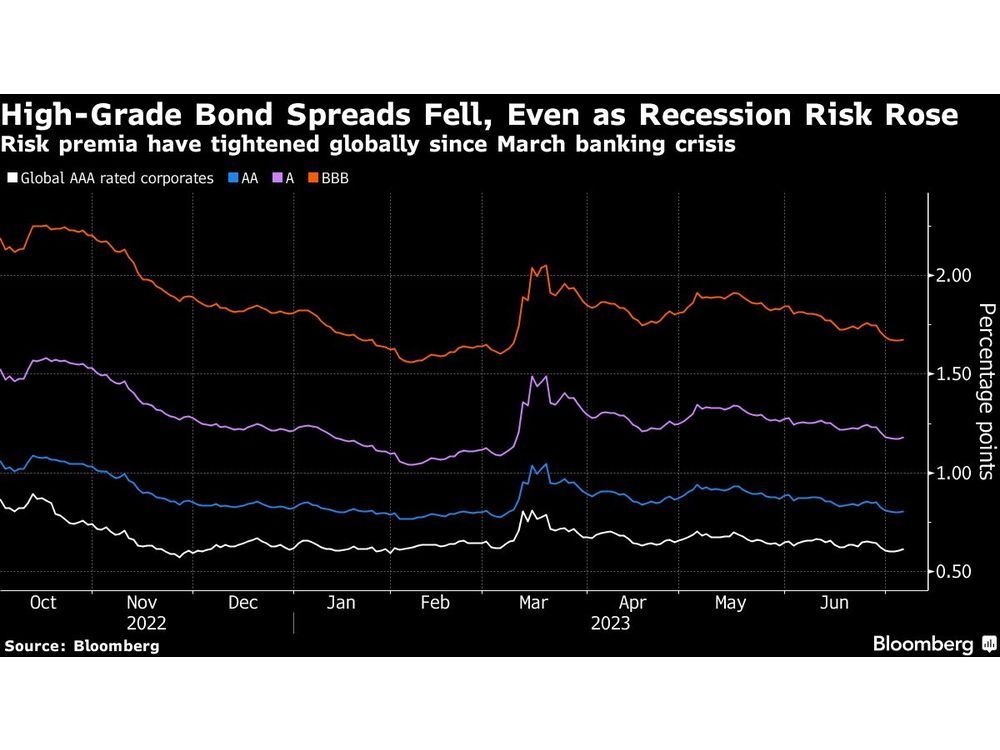

Yet, investors don’t necessarily price it in. Growing demand for debt from global majors has cut the extra yield you pay on government bonds, or spreads, to the lowest level since March, when the US regional banking crisis hit global credit markets.

“The higher interest rates that are absorbed by the economy will start to show up on the income statements of investment grade companies,” said David Knutson, chief investment director at Schroders plc. “The economy will continue to slow gradually, and a slowing economy generally means wider margins.”

Article content

Advertising 3

Article content

Any downturn would be painful for companies that have accumulated massive amounts of cheap debt in recent years. And as companies refinance, those loans risk becoming a millstone. More than $500 billion of BBB-rated bonds, or two steps above junk status, are at risk of a ratings downgrade, according to an analysis by Bloomberg Intelligence last month.

weaker metrics

“Metrics of cash flows and profit margins were weaker in almost all sectors,” said Joel Livington, director of credit research at BI, after reviewing nearly 1,450 issuers. “If business trends continue, you will end up with weaker leverage metrics like debt/Ebitda. And that could have implications for valuations.”

More companies being downgraded to junk would also make it more difficult for existing speculative-rated companies to raise liquidity and could lead to a rise in defaults.

Advertising 4

Article content

UBS Group AG last month predicted defaults on highly leveraged loans and junk bonds would reach 8% and 6%, respectively, in early 2024.

Even executives at investment-grade companies seem to be preparing for a turnaround in the economy. Citigroup analysts note that buybacks as a percentage of EBITDA are already declining, as is dividend when compared to the same metric.

more conservative

“Trends in returns of equity to shareholders indicate that IG companies are becoming more conservative in using cash ahead of a potential downturn,” the analysts wrote.

Others are more positive about expectations. “The well-telegraphed pending recession that has yet to materialize has resulted in many companies remaining conservative in their growth plans and balance sheets, leaving them in a better position than we typically see late in the year,” said Travis King, US chief investment officer. session”. Tier 1 companies at Voya Investment Management.

Advertising 5

Article content

However, the economist at Apollo Global Management Inc. notes: Torsten Slok pointed to an increase in recent weeks in the number of companies with obligations of $50 million or more seeking bankruptcy protection as a sign that a cycle of defaults may have begun in the broader credit market.

“Maybe interest rate increases are starting to come,” he said, adding that “the Federal Reserve is succeeding in slowing the economy.”

a week in review

- Private equity firms have to reduce leverage in acquisitions to get deals done, hoping to add more debt later.

- After disrupting financing markets by wringing buyout debt deals from Wall Street, private credit firms are now changing the landscape in part of the $1.3 trillion CLO business.

- Auto loan-backed bonds are heading for their first loss since the 1990s as Americans default on payments and dealerships collapse.

- The ESG funds that have accumulated green bonds being sold by Thames Water Plc are trying to figure out what environmental, social and governance disasters threatening the future of utilities mean for their holdings.

- Rallye SA, the holding company that controls the ailing grocery casino, faces a 25 million euro ($27.2 million) fine after regulators in the French market accused it of artificially inflating the price of its shares by being deceived about its access to cash.

- State-backed construction company Sino-Ocean’s dollar bonds have almost halved in a week, after news that its shareholders had set up a working group to look into its debt and hire a financial advisor.

moves

- Wells Fargo & Co. has appointed Two highly productive salespeople at Credit Suisse Group AG are Brian Harris and Emma Bramson.

- Teresa Debenedictis, a loan sales representative at UBS Group, has left the Swiss lender after working there for more than 25 years.

- Adam Russell, a corporate credit dealer at Royal Bank of Canada, has left the bank, while three new employees have joined the European debt capital markets team, including Alex Ulrich and Eugen Eichwald in Frankfurt.

comments

Postmedia is committed to maintaining an active and civil forum for discussion and encouraging all readers to share their opinions on our articles. Comments may take up to an hour to be moderated before they appear on the site. We ask that you keep your comments relevant and respectful. We’ve enabled email notifications – you’ll now get an email if you get a response to your comment, if there’s an update to a comment thread you’re following or if it’s a user you’re following. Visit our Community Guidelines for more information and details on how to adjust your email settings.

Join the conversation