Artificial intelligence (AI) and semiconductor chips have captured the collective imagination of investors — and with good reason. Together, they drive the technology of the future. Semiconductor chips are ubiquitous in our digital age, and in recent months artificial intelligence has begun to change the way we communicate with our devices. The convergence of these two fields means unlimited possibilities.

For investors, this is particularly exciting. The Philadelphia Semiconductor Index, PHLX, which tracks the chip sector by the performance of the 30 largest semiconductor manufacturers, has gained nearly 39% so far this year.”

PHLX for good reason. Semiconductors have been here for decades, and they are in almost everything in today’s digital world, but together with artificial intelligence, they will drive the technology of tomorrow. Investors have picked this up, and made chipmakers the best AI shares.

The question now is, how much room should AI chip stocks grow? We can consult Street’s analysts – several top equity professionals have been weighing in on AI and semiconductors, and their comments can shed more light on the sector. Let’s take a look at what they have to say, and which AI-related giants they recommend.

Nvidia Corporation (NVDA)

The first is Nvidia, a major name in the semiconductor industry, the eighth largest chip maker by revenue. Nvidia is a leading manufacturer of Graphics Processing Units (GPUs), and has built its reputation on these cutting-edge chips. The chips are capable of handling the computing power needs of many high-end, processing-intensive applications, including professional graphic design, high-end gaming — and artificial intelligence. Demand for Nvidia’s GPUs, especially in the latter application, fueled the stock’s strong gains this year; Year-to-date, NVDA shares are up nearly 190%.

Recent data shows that Nvidia’s performance stands on its AI products. OpenAI, the company that launched ChatGPT, has been using Nvidia’s GPUs since 2020 to train its AI units – as many as 20,000 chips. Looking ahead, OpenAI has indicated that it may need another 10,000 slices to keep ChatGPT efficient.

This is a solid foundation for Nvidia’s success, and the company’s strong position can be inferred from the strong rout it posted in its recent first-quarter financial results. This report showed total top line revenue of $7.19 billion. While that was down 13% from the previous year, it beat expectations by about $670 million. The core number, non-GAAP earnings per share of $1.09, was 17 cents per share better than expected.

Even better, from an investor standpoint, is Nvidia’s guidance. The company expects sales of $11 billion in the fiscal second quarter, which is a huge increase from its previous guidance of $7.2 billion. Achieving this will translate into a 41% year-over-year increase in quarterly revenue.

This company’s strength in AI underlies optimistic comments from five-star analyst Joseph Moore at Morgan Stanley, who wrote: “NVDA should trade at a premium to peers given the greater likelihood of upward revisions in the near term, but multiple premiums versus premiums.” These peers have dwindled significantly… However, we do see continued growth in NVDA’s data center business, on a multi-year trajectory that should clearly be above all other compute players on a compound basis, given the lack of offsetting or cannibalizing the compute business out field of artificial intelligence.

The analyst added, “As a result, we see NVDA as the cleanest story in AI hardware, and we believe it still deserves more attention from investors looking for exposure to AI, even if the composition of the current valuation and stock return to date already reflects the expectations that are.” higher than the minor or tertiary players.”

To that end, Moore placed an Overweight (i.e. Buy) rating on NVDA, which he upgraded to be his top pick. In Moore’s view, NVDA will hit $500 by this time next year, which would mean an 18.5% gain from current levels. (To watch Moore’s track record, click here)

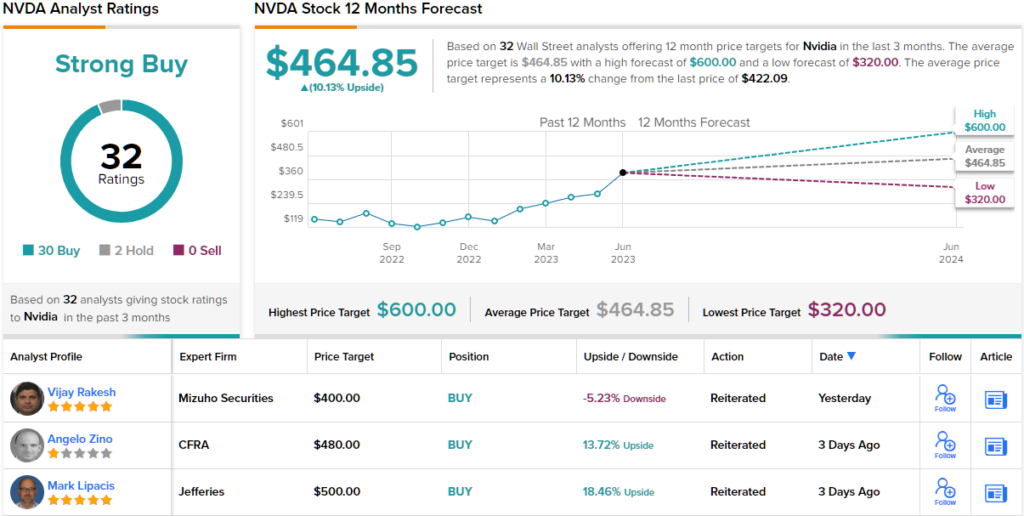

Overall, Nvidia has a Strong Buy rating from the Wall Street analyst consensus, based on 33 recent reviews that split into 30 Buys versus just 3 Holds. Shares are trading for $422.09, and the average price target of $464.85 suggests a modest upside of 10% in the next 12 months. (be seen NVDA Stock Outlook)

advanced micro devices (AMD)

AMD, in terms of sales, is always one of the top ten chipmakers, and has seen total revenue of $23.06 billion in the past four quarters (2Q22 through 1Q23). The company has a market capitalization of $188 billion and has a broad portfolio in the AI ecosystem, including high-performance chips and architectures.

AMD’s AI exposure includes Instinct GPU accelerators, Alveo Adaptive accelerators and EPYC server processors, as well as several lines of chips, including Ryzen AI mobile processors, and Adaptive Core Versal AI SoCs. Found in a wide variety of applications, from gaming to data centers to supercomputers, AMD AI chips and accelerators provide the processing speed and capacity needed for generative AI.

In numbers, the company’s recent performance has been better than expected. In the first quarter of this year, AMD showed $5.35 billion in total revenue. And while that was down about 9% year-over-year, it beat expectations by $40 million. The company’s non-GAAP net profit of 60 cents a share also beat expectations, 4 cents short of estimates. On the downside, the company’s second-quarter revenue guidance of $5.3 billion was considered weak, falling short of expectations of $5.52 billion.

The company’s AI portfolio provides an important support to the company. AMD is shifting its strategic focus to the emerging AI market, and is investing heavily in both networking and data center AI operations. Getting to the details, AMD’s new Ryzen 7000 series includes AI processing capabilities, and the MI300 chips are designed for both high-performance computing and AI applications. The latter path will find support from the rapidly growing field of generative AI.

These are the main points behind Baird analyst Tristan Gera’s comments on AMD. Gira, who has a 5-star rating from TipRanks, says of the company: “The Mi300x claims best-in-class TCO performance for inference applications, and management has reiterated its forecast for meaningful AI revenue starting in Q4 2023 based on several superior shares. AMD sees a compound annual growth rate of more than 50% to accelerate data center AI by 2027, to $150 billion + TAM.While its ecosystem is not as mature as Nvidia, AMD is well positioned to be a major beneficiary of secular growth trends for AI in the medium term, in our opinion.”

Based on the above, Gerra assigns an outperform (i.e. Buy) rating to AMD stock, and gives the stock a price target of $170 to indicate an upside potential of 54.5% over the 12-month horizon. (To view the Jira log, click here)

Overall, Street gives AMD a Moderate Buy consensus rating, based on 29 recent analyst reviews that include 21 Buys and 8 Holds. The stock is currently trading at $110.01 and the average price target of $134.31 indicates that it will rise 22% in the next year. (be seen AMD stock outlook)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best stocks to buya tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.