The US dollar rebounded today after reacting to a higher preliminary 1-year University of Michigan inflation forecast and generally better data from the monthly consumer survey. Yields have also risen sharply.

The inflation reading showed a modest increase from 3.3% to 3.4%. However, the market which responded positively to better CPI and PPI data this week, with the least gains, ruled out a bit of “inflation moving lower”. Actual sentiment indexes were also sharply higher with:

- Consumer confidence rose to 72.6 from 64.4 last month.

- Current conditions rise to 77.5 from 69.0 last month, and

- Forecasts rose to 69.4 from 61.5 last month.

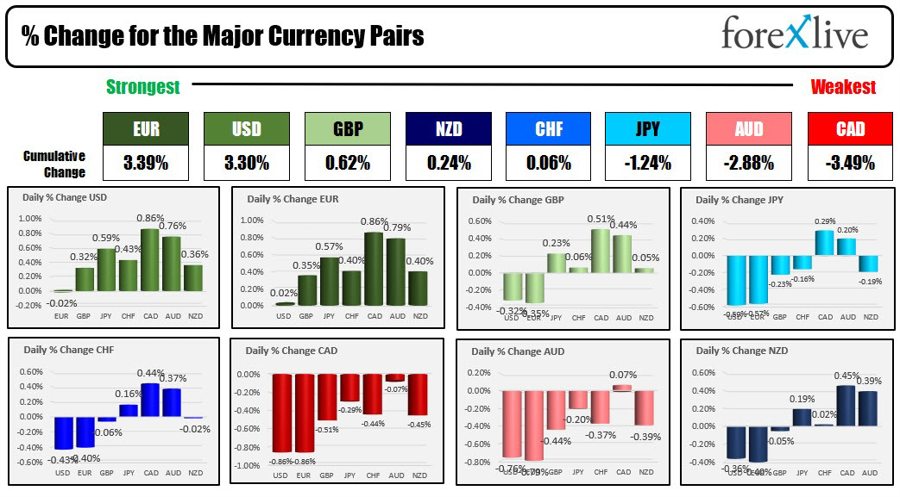

Looking at the strongest to the weakest, the euro has dumped the US dollar against the strongest of the majors (the dollar is down -0.02% against the euro), but the greenback has made decent gains against the other currencies. The dollar made its biggest gains against the Canadian dollar (+0.86%) and the Australian dollar (+0.76%). The US dollar also rose against the Japanese yen by 0.59%.

From the strongest to the weakest among the major currencies

Although it rose today, the US dollar ends the trading week with a decline against all major currencies. Here are the changes for majors:

- Euro, -2.34%

- GBP -1.98%

- Japanese yen, -2.38%

- CHF, -3.06%

- Canadian Dollar, -0.46%

- AUD -2.15%

- NZD -2.60%

Low inflation from CPI and PPI this week gives traders hopes that the Fed will have only one additional hike in 2023, despite some overtures that 2 remains the most likely scenario from some Fed officials including Daley and Waller of the Federal Reserve Bank.

The Fed’s Waller said the September meeting is still “live” (most expect the Fed to skip that one), but still sees “two more 25 basis point increases in the target range over the four remaining meetings this year necessary to keep the Fed moving.” Inflation is toward our target,”

The Fed’s Daly said earlier this week (before the inflation data) that a two-fold hike is still likely. Yesterday, she backtracked a bit, saying that the comments earlier in the week were intended to keep the electives open for an additional raise this year.

The Fed then announces its interest rate decision on July 26th. The September meeting will be held on September 20th and the November meeting on November 1st. This allows for two additional readings of unemployment and inflation before the September meeting, and three more readings before the November meeting. Obviously, this data will be enough to see if the decline in inflation has continued its course and moved upwards again, or if it continues to decline.

This week the market was full of optimism about the Goldilocks economy with growth staying but inflation coming down.

In today’s US bond market, yields have corrected higher after falling earlier this week. For the day:

- 2 years yield 4.767% +15.7 basis points

- 5-year yield of 4.045%, +11.0 basis points

- 10-year yield of 3.830% +7.1 basis points

- 30-year yield of 3.925% +3.1 basis points

For the trading week, returns were still down:

- The two-year yield decreased by 17.8 basis points

- The 5-year yield decreased by 31 basis points

- The 10-year yield decreased by 23 basis points

- The 30-year yield decreased by 11.7 basis points

Lower yields and a lower dollar – along with the Goldilocks scenario – helped boost stocks this week:

- The Dow Industrial Average added 774 points, or 2.29%.

- The S&P added 106.45 points, or 2.42%.

- The Nasdaq added 452.98 points, or 3.32%.

Nasdaq’s gain was the largest since the week of March 27, 2023.

In Europe, most major indices were lower today, but like US indices, they posted strong gains for the week:

- German DAX +3.22%

- Francis Kak + 3.69%

- UK FTSE 100 Index, +2.45%

- Spanish Ibex, +2.05%

- Italian FTSE MIB Index, +3.19%

In the Asia Pacific market:

- Japan’s Nikkei 225 rose 2.42%

- Hong Kong’s Hang Seng Index rose 5.71%.

- China’s Shanghai Composite Index rose 1.28%.

- Australian S&P/ASX rose 3.7%

European benchmark 10-year yields fell sharply:

- Germany, -15.9 bps

- France, -15.2 bps

- UK, -27.3 bps

- Spain -15.7 basis points

- Italy -18.6 basis points

The Canadian 10-year yield fell -20.7 basis points this week.

Next week, US earnings season will continue with more big financial releases including:

- American bank

- Morgan Stanley

- Charles Schwab

- PNC Finance

- Bank of New York

- Goldman Sachs

- American Express

There will be a number of regional banks that are believed to be more likely to report earnings volatility. Of the 15 largest stocks in the regional banks’ KRE ETF, 12 will account for about 25% or the index (I think I’ve heard that 60% of the KRE will go public next week).

Among the other big names to announce next week are:

- Tesla, Netflix and IBM on Wednesday

- Johnson & Johnson, American Airlines, United Airlines and Travelers will announce Thursday

I look forward:

- Alphabet is scheduled for Monday, July 24th

- Microsoft is scheduled for Tuesday, July 25th

- Amazon, Meta, and Boeing are scheduled for Wednesday, July 26

- Bristol-Myers Squibb, Intel, McDonald’s, and Northrop Grumman due Thursday, July 27

Here is a summary of some of the major economic releases (times are ET)

Sunday 16th July

- 10:00pm: China GDP for the second quarter (forecast: 7.1%, previous: 4.5%)

- 10:00pm: China Industrial Production YoY (Forecast: 2.5%, Previous: 3.5%)

Monday 17 July

- 8:30 am: US Empire State Manufacturing Index (forecast: -3.5, previously: 6.6)

- 9:30 pm: Australian monetary policy meeting minutes

Tuesday 18 July

- 8:30 am: Canadian CPI on a monthly basis (forecast: 0.3%, previous: 0.4%)

- 8:30 am: Canadian CPI median year over year (forecast: 3.7%, previous: 3.9%)

- 8:30 am: Canadian CPI contracted yoy (forecast: 3.6%, previous: 3.8%)

- 8:30 am: Core US Retail Sales MoM (Forecast: 0.4%, Previous: 0.1%)

- 8:30 am: US Retail Sales Monthly (Forecast: 0.5%, Previous: 0.3%)

- 6:45 pm: New Zealand CPI quarterly (forecast: 0.9%, previous: 1.2%)

Wednesday 19 July

- 2:00 am: UK CPI YoY (Forecast: 8.2%, Previous: 8.7%)

- 9:30pm: Australian Employment Report (Forecast: 16.5K, Previous: 75.9K)

- 9:30 pm: Australia’s Unemployment Rate (Forecast: 3.6%, Previous: 3.6%)

Thursday 20 July

- 8:30 am: US jobless claims (forecast: 242k, previous: 237k)

Have a great weekend.