Centennial Holdings (CELH) – Get a free reportIt was already growing rapidly before it signed a distribution deal with PepsiCo (PEP) – Get a free reportlast fall. Now that Pepsi’s reach has been leveraged to enter more stores and win additional shelf space at existing locations, revenue and profits are increasing exponentially. Given that many companies are struggling to expand sales and profits, are Celsius shares worth owning in your portfolio?

A look back at Celsius Holdings’ business

Celsius Holdings is a beverage company that is rapidly gaining market share in the energy drink market. Selling highly caffeinated beverages is a good business. The US energy drink market grew at a compound rate of 11% annually between 2017 and 2022, reaching $18.9 billion last year, according to IBISWorld.

The global market opportunity is much greater. In 2021, energy drinks are brought in $159 billion worldwideAccording to Statista. It is estimated that worldwide sales will rise to $233 billion by 2027.

The biggest players in the industry in terms of market share are Monster (mnst) – Get a free reportand Red Bull, but Percentage is steadily declining in market share. Over the past year, Celsius has been the fastest growing multi-outlet and convenience store (MULO-C) energy drink in the United States. As a result, Celsius Holdings became the third largest maker of energy drinks in the United States with a market share of 7.5%, double its share from a year ago.

According to SPINS’ consumer product tracker, Celsius sales grew 124% year-over-year in the last four weeks of the first quarter, much faster than the 12.4% annual growth for the energy drink category.

The percentile financials are solid

With the company’s products selling in more stores thanks to its deal with Pepsi, and sales growing in the first quarter at a triple-digit pace, it’s no surprise that revenue is up so dramatically.

In the first quarter, Celsius Holdings reported Sales grew 95% to $260 million. North American revenue rose 101% to 249 million, accounting for the lion’s share of sales. Overseas, sales increased 15% to $11.4 million.

The company’s underlying performance was similarly positive. Gross margin expanded 3.4% to 43.8%, and with sales-driven operating leverage, earnings per share jumped 344% to $0.40.

The balance sheet looks solid as well. Celsius Holdings ended the quarter with $614 million in cash and cash equivalents and just $161 million in current liabilities. It carries very little debt, with current and long-term debt totaling only $731,000 and $488,000, respectively. As a result, his current ratio is 5.18 – well above the 1.0 level most people would consider alarming.

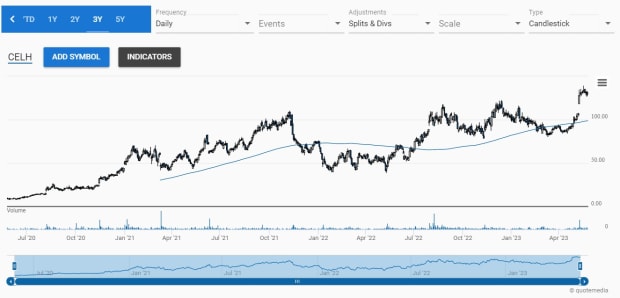

Attractive holdings percentage chart

Celsius Holdings is trading above $131, which puts the stock well above its bullish 21-day, 50-day, and 200-day moving averages.

real moneyBruce Kamich of Bruce Kamich has professionally evaluated charts for nearly 50 years. Last week, it is impressed According to what he saw on Celsius Holdings candlestick charts.

Kamish noted that Celsius Holdings stock has been rising for three years. Its share price is above its 40-week moving average rising, Balanced Volume (total running up minus down) is positive, and its Moving Average Convergence Divergence Momentum Index is bullish.

Based on Celsius Holdings’ weekly point-and-number chart, Kamich calculated a price target of $232, well above where the shares are currently trading.

Is Celsius Holdings Stock a Buy?

The company has a lot of things going its way. More people are consuming energy drinks instead of soda and percent energy drink ingredients, and marketing is positioning them as a potential healthier source of caffeine. Revenue and earnings are rising quickly, which is attractive based on technical analysis.

One drawback is that Celsius Holdings shares aren’t cheap. Analysts expect EPS to grow 50% next year to $1.96, but a higher after-earnings report has pushed the forward price-to-earnings ratio above 67. That’s far from bargain pricing, since Monster’s forward price-to-earnings ratio is 32. Pepsi is 23 years old. However, Celsius Holdings is growing much faster than those companies, so the premium rating is understandable. However, this stock is not likely to attract value investors.

However, growth investors may want to use any pullbacks to buy stocks. The company is already growing rapidly, however the overseas market opportunities are basically untouched and there is also an opportunity to expand Silesian beverages in restaurants.

Another reason why Celsius Holdings stock is a good buy? It can be said that it is wholly owned by mutual funds and hedge funds. Shares appeared in 529 funds, up from 399 a year earlier. For perspective, the 1940 funds own shares in Monster. Since Percentage hasn’t caught the eye of many institutional investors, it might be smart to buy the stock.