The upcoming week is expected to be relatively quiet, with a handful of economic events drawing attention.

On Tuesday, in Australia, the RBA is set to announce the Cash Rate and release its Rate Statement.

Moving to Wednesday, New Zealand will reveal its Inflation Expectations quarter-on-quarter (q/q), while in the U.K., BoE Governor Bailey is scheduled to deliver a speech at the Central Bank of Ireland Financial System Conference, held in Dublin.

Later in the day, in the United States, Fed Chair Powell will deliver opening remarks at the Division of Research and Statistics Centennial Conference in Washington, D.C., although this speech is not expected to create market volatility, but it’s worth monitoring for any potential insights. As a reminder, the Fed decided to keep its monetary policy unchanged at the last meeting. Given the latest labor market data, it appears that the current hiking cycle may have reached its peak. While the possibility of one more hike remains, many analysts believe it won’t materialize until the year’s end. However, until the next FOMC meeting in December there will be two more CPI data releases and one final labor market report which could influence the Bank’s decision.

On Thursday, the U.S. will release data on unemployment claims. Powell is also scheduled to speak in a panel discussion titled “Monetary Challenges in a Global Economy” at the Jacques Polak Annual Research Conference, in Washington, D.C.

Finally, Friday will bring the United Kingdom’s GDP for the month as well as the Preliminary GDP q/q. Meanwhile, in the U.S., the Preliminary UoM Consumer Sentiment and Preliminary UoM Inflation Expectations will be reported. Throughout the week, seven Federal Reserve members are scheduled to deliver their remarks which could reveal their thoughts on how the rise in Treasury yields has impacted financial conditions.

In the forthcoming RBA meeting this week, there is a high probability that the Bank will opt for a rate hike. Recent inflation growth in Australia makes it hard to bring inflation into the Bank’s desired target range of 2-3%. Given the RBA’s expressed concerns about elevated inflation levels, it’s likely that the newly appointed Governor, Michelle Bullock, will choose to raise the cash rate by 25bps to 4.35%, as suggested by analysts from ING.

Survey data from New Zealand indicates that inflation expectations for the next two years are softening. While the RBNZ would prefer a faster decline, it appears that the process is occurring gradually at a slower pace. Borrowing costs continue to increase, pushing inflation down, but for now it’s not enough to bring it in line with the Bank’s target of 2%.

On Thursday, the United States is set to release data on unemployment claims and the consensus is for a rise from 217K to 218K. Data has shown a slight upward trend recently, but the initial claims figure remains at a low level, potentially indicating that businesses are not yet under significant pressure to lay off employees, according to ING analysts.

The U.K. is set to release its GDP data this week. The most recent monthly figures indicate that the quarterly GDP is likely to show a negative reading, with the consensus projecting a decline from 0.2% to -0.1%. The BoE continues to anticipate a period of stagnation, but since the start of the year, the U.K.’s economic outlook has shown signs of improvement. There is a potential for economic conditions to further recover in the upcoming quarters; however, the risk of a recession has not been completely averted.

The recent decline in U.S. consumer sentiment may be attributed to various factors, including labor strikes and the ongoing situation in Israel and Gaza, which have generated uncertainty. The consensus anticipates a further decrease in consumer sentiment from 63.8 to 63.4, but might see a bounce back caused by decreasing gasoline prices which heavily influence cost of living.

Regarding inflation expectations, the data from the previous month indicated preliminary year-ahead inflation expectations rising to 4.2%, with long-term inflation expectations also increasing to 3%. However, it’s worth noting that despite the recent jump, expectations for the following year may decrease if inflation continues to go down.

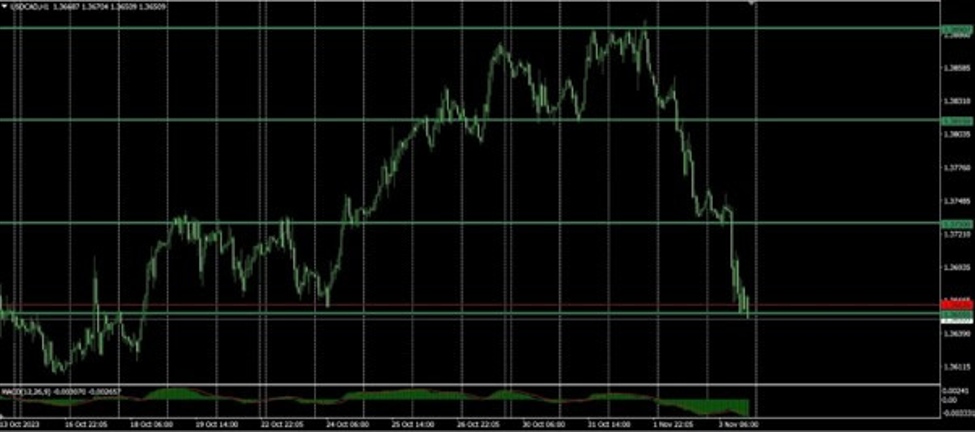

USD/CAD expectations

On the H1 chart the pair closed the week near the 1.3655 level of support. From there a correction is expected until the 1.3730 resistance and if that level doesn’t hold, the next target could be 1.3580.

On the upside, the next levels of resistance are at 1.3815 and 1.3890.

From a fundamental point of view the latest U.S. labor market data and the outcome of the last FOMC meeting confirmed what the market was anticipating: Some softness in the U.S. economy and the fact that the hiking cycle might have reached its peak. This is not good news for the USD, but it will help the CAD strengthen in the short term.

There is a light week in terms of economic events for both the USD and the CAD. On Wednesday the BoC Summary of Deliberation will be released, but it’s not expected to provide clues about policy outlook which means it will not impact the Canadian dollar.

USDCAD 1 hour

This article was written by Gina Constantin.