(Bloomberg) — It’s been a tough couple of years for real estate stocks since the Federal Reserve began raising interest rates in 2022, with borrowing costs rising and the real estate market collapsing. Despite a healthy recovery in mid-2024, the outlook for 2025 is not particularly encouraging.

Most read from Bloomberg

But that doesn’t mean investors should expect a sea of red in real estate stocks next year. Instead, it’s likely a stock-picking market, where some rise, others fall, and the group doesn’t move in perfect unison, according to Adam White, senior equity analyst at Truist Advisory Services.

That’s not great news for the residential market, which is expected to face challenges from stubbornly high mortgage rates and limited supply in 2025, especially after Federal Reserve Chair Jerome Powell’s comments on Wednesday suggesting fewer interest rate cuts. The average interest rate on a 30-year fixed mortgage rose this week for the first time in a month, Freddie Mac said in a statement Thursday.

But there is growing optimism in one of the most beaten-up corners of the market: office REITs.

“Where REITs can really compete is in their cost and availability of capital, and that may be the case for offices,” said Uma Moriarity, chief investment strategist at CenterSquare Investment Management. “When you think of a premium asset in any given market, it’s likely to be owned by a REIT.”

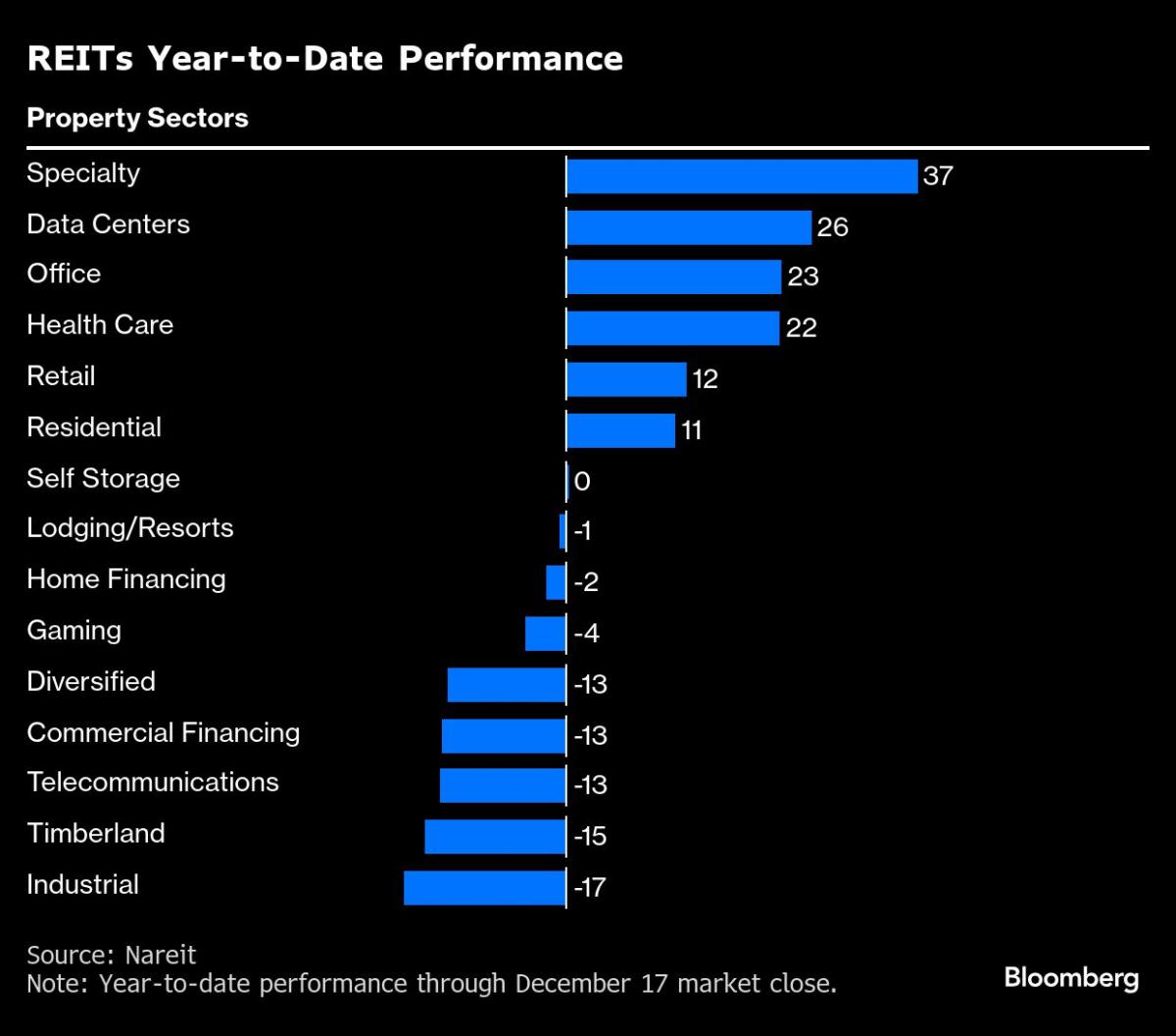

The group has taken a hit since the start of 2022, with the S&P Composite 1500 Office REITs index falling more than 30% while the S&P 500 index is up 24%.

This difference is not entirely shocking given the headwinds facing the real estate industry along this stretch. The cost of borrowing rose as the Federal Reserve raised interest rates 11 times between March 2022 and July 2023, the regional banking crisis of March 2023 crippled local lenders, and employers struggled to force workers to return to their offices after coronavirus lockdowns.

Office recovery

These pressures have led to a decline in real estate stocks across the board. U.S. REITs have been cheap or less expensive than the S&P 500 11% of the time over the past 20 years, according to Todd Kellenberger, a REIT client portfolio manager at the major asset manager. Office REITs are still down about 60% from pre-Covid levels compared to the rest of the REIT market, making them a decent target for growth, according to Moriarity.

Comments are closed, but trackbacks and pingbacks are open.