This week’s calendar was action packed, prompting our FX strategists to focus on shorter-term ideas and very specific fundamental and technical triggers.

We think it was a net neutral performance week with only one day where our discussion clearly and easily played out, and the other two highly dependent on risk/trade management due to the choppiness in markets all week.

If you’d like to follow our “Play of the Day” picks right when they are published throughout the week, you can subscribe to BabyPips Premium.

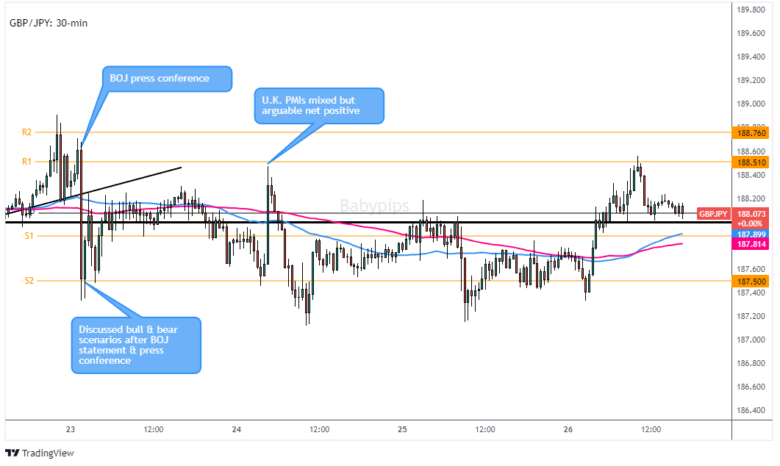

For our first strategy discussion of the week, we looked at GBP/JPY as it had several major catalysts at play, including the latest monetary policy statements from the Bank of Japan and the upcoming flash purchasing managers survey data from the U.K.

We discussed both bull and bear potential scenarios, and after we got relatively upbeat remarks from BOJ Governor Ueda, we thought that if we saw a break below the Pivot Point level, sellers may jump in and push the pair to the Pivot S1 (187.88) or even S2 (187.50) areas.

After our post, it looks like traders stayed net positive on the Japanese yen all week as every dip in JPY seemed to draw in net buyers (and making it the best performing currency after the , likely on the idea that the BOJ will eventually end negative interest rates sometime this year.

Even when we saw a net positive U.K. flash PMI read and GBP/JPY pop higher, that was once again a shorting opportunity to play the big JPY theme that has been developing over the past few months.

For those stayed bearish on GBP/JPY after the BOJ press conference and shorted on the bounces around the Pivot Point area and had wide enough stops to withstand event volatility, its highly likely you saw a positive outcome, especially since we saw multiple moves to our target support areas during the week.

For those who flipped bullish on GBP/JPY after the U.K. PMI updates, it’s likely you saw a negative outcome if you bought after the event. But for those who used that event outcome as their directional thesis on GBP/JPY and waited for dips below the pivot, it’s possible you saw positive outcomes, especially if entering around the S2 line, which was tested and held three times after the U.K. PMI event.

Overall, the performance of this discussion was arguably neutral-to-effective as our discussed bearish scenario did play out and targets were hit, but the outcome would have highly likely depended on an individual’s trade and risk management strategies used given the choppiness of the pair all week.

On Wednesday, we looked at USD/CAD ahead of likely volatility due to the latest monetary policy statement from the Bank of Canada. As usual, we made cases for potential bull and bear scenarios, as well as citing potential profit targets depending on the event outcome and initial market reaction.

The event did not disappoint as it definitely brought the volatility, thanks to the BOC essentially taking rate hikes off the table if inflation and growth outlook/data remain inline, but did push back on rate cuts a bit.

USD/CAD immediately spiked higher on the event, and moved to our upside targets (the 1.3485 area of interest near R1) pretty easily. The pair actually got up as high as 1.3534, before traders started taking profit, repositioning ahead of U.S. events, essentially giving back control to the sellers.

Given that our fundamental bull scenario played out as described and our upside resistance target was hit, we make a strong argument that this was a very effective discussion towards a positive outcome, especially for those who managed their trade to go for higher targets and managed the trade/risk ahead of the highly anticipated U.S. data.

Finally on Thursday, we focused mainly on the U.S. dollar as the probability of volatility spikes was high due to top tier U.S. events on the way. The pair had been in consolidation mode all week, so we thought there was a possibility these events may create a consolidation-breakout setup in either direction. Unfortunately for swing traders, both events turned out to be duds in terms of sparking a massive move in the Greenback.

First, the GDP read did give a positive surprise that boosted USD higher, but that was quickly tempered by the net disappointing weekly U.S. initial jobless claims and durable goods data, and the fall in the GDP price index. This actually was a potential scenario discussed in the post where a good short-term strategy to consider would be to fade the initial GDP price reaction and target pre-event price levels.

Second, the Core PCE Price Index data was not a major market mover, likely due to no major surprises in actual vs. expectations and the metrics conflicting with each other on different time frames. The monthly read ticked higher from 0.1% m/m to 0.2% m/m while the year-over-year read dipped from 3.2% to below expectations at 2.9% y/y.

Personal income and spending data was released at the same time and was arguably mixed as well as the rise in incomes dipped from 0.4% to 0.3% in December, while spending rose significantly from 0.4% to 0.7%, likely due to the holidays.

Based on the price action, the results were taken as a net positive for the U.S. dollar, signaled by the rally through the end of the Friday session against all of the majors.

So with this discussion, from short-term standpoint, this may have lead to a positive outcome if GDP reaction fade idea was executed on. But overall, we’d rate this discussion as a neutral as we didn’t get the price reactions and consolidation break to trigger a legitimate play in either direction.

But given the Greenback’s performance this week and the event outcomes, this consolidation is something to watch, especially with the FOMC set to give their latest monetary policy statement this week!