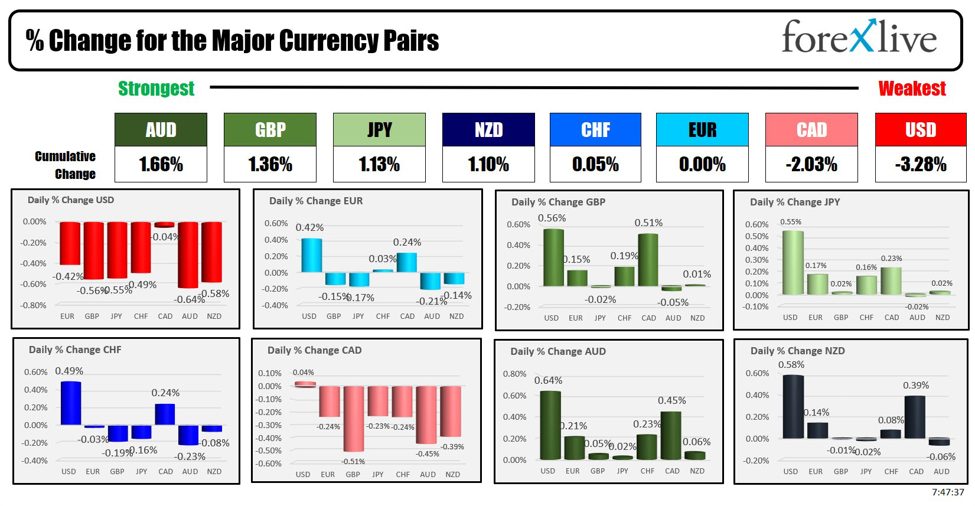

As the North American session began, the Australian dollar was the strongest followed by the British pound, with the US dollar the weakest. The Federal Reserve will meet on Tuesday and again on Wednesday before announcing its interest rate decision on Tuesday at 2 p.m. ET. A press conference will begin at 2:30 with Fed Chairman Powell. The odds of a 50 basis point rate cut have gained momentum since Thursday and are now roughly a 50-50 chance.

The Bank of England and the Bank of Japan are also scheduled to meet this week.

Central Bank Comments Over the Weekend and Today (Fed in Quiet):

Last week, the European Central Bank met and cut interest rates. As with the previous cut, the ECB appears to be “pre-determined” (or perhaps strongly inclined) to keep rates unchanged at the next meeting (despite saying otherwise).

- European Central Bank policymaker Peter Kazimir has indicated that the central bank is likely to wait until December to cut interest rates, noting that it would take a significant change in the economic outlook for a rate cut in October. With little new information expected before the October meeting, Kazimir stressed that there is no urgent need to cut rates and suggested that the safest approach is to wait until the economic outlook becomes clearer.

- European Central Bank Vice President Luis de Guindos said in Madrid that the ECB’s forecasts indicate that inflation will be around 2% by the end of 2025. He expressed concern about the persistence of inflation in the services sector, noting that the ECB does not have a pre-determined path for interest rates, stressing that decisions will be taken on a meeting-by-meeting basis.

- The European Central Bank’s Chief Economist Philip Lane said that recent data on wages and profits were in line with expectations. He noted that negotiated wage growth is expected to remain high and volatile for the rest of the year. Lane stressed that a gradual approach to easing policy constraints would be appropriate if future data were in line with the ECB’s core expectations, while also highlighting the need to maintain flexibility regarding the pace of policy adjustments.

The Bank of Canada cut interest rates by 25 basis points at its last meeting:

- In an interview with the Financial Times, Bank of Canada Governor Tiff Macklem raised the possibility of a faster rate cut, reflecting his growing concerns about the state of the labour market. Macklem noted that the labour market is showing signs of downside risks, which could weigh on the broader economic outlook. He stressed that with inflation approaching the bank’s target, there is a growing need to be vigilant about potential downside risks, suggesting that a more cautious approach may be necessary in future monetary policy decisions.

Greg Ip of the Wall Street Journal gave his opinion on the Fed, saying:

- The Fed should cut interest rates by 50 basis points instead of the expected 25 basis points at its next FOMC meeting on September 18. Ip suggests that the primary focus should be on where interest rates should be, which he believes is well below their current level. He argues that inflation is under control and there is little sign of an impending recession. However, he cautions that waiting for concrete signs of a recession could be risky, meaning that a more aggressive rate cut would better preempt potential economic challenges.

A quick snapshot of other markets as the North American session begins:

- Crude oil price rose $0.52 to $69.72. At this time yesterday, the price was at $68.30.

- Gold rose $4.93, or 0.18%, to $2,567.00. At this time yesterday, the price was $2,517.84.

- Silver prices rose $0.16 or 0.53% to $29.99. At this time yesterday, the price was $28.75.

- Bitcoin is trading at $58,336. At this time yesterday, the price was at $58,026.

- Ethereum is trading at $2371.50. At this time yesterday, the price was at $2348.70.

In pre-market trading, the picture for major indexes was mixed after Friday’s gains. Both the S&P and Nasdaq are on a five-day winning streak.

- Dow Jones Industrial Average futures point to a gain of 100.23 points. On Friday, the index rose 297.01 points, or 0.72%, to 41,393.78.

- S&P 500 futures point to a -4.71 point decline. On Friday, the index was up 30.26 points, or 0.54%, at 5,626.02.

- Nasdaq futures point to a -83.22 point decline. On Friday, the index rose 114.30 points, or 0.65%, to 17,683.98

The Russell 2000 small-cap index rose 53.06 points, or 2.49%, to 2,182.49 yesterday.

European stock indices trade little changed at the start of the week:

- German DAX, -0.25%

- French CAC index -0.04%

- UK FTSE 100, +0.08%

- Spanish IBEX, +0.14%

- Italian FTSE MIB, -0.04% (10 min delayed).

Stocks in Asia-Pacific, Japan and China markets were closed for holidays.

- Japan’s Nikkei 225, bank holiday

- China’s Shanghai Composite Index, Bank Holiday

- Hong Kong’s Hang Seng Index, +0.31%.

- Australia’s S&P/ASX, +0.27%.

Looking at the US debt market, yields have not changed much:

- The yield on the two-year note was 3.546%, -2.9 basis points. On the same Friday, the yield was 3.597%.

- The yield on the 5-year Treasury note is 3.407%, -1.7 basis points. At this time Friday, the yield was at 3.432%.

- The yield on the 10-year note is 3.636%, -1.3 basis points. At this time on Friday, the yield is at 3.653%.

- The yield on the 30-year Treasury note is 3.962%, -1.5 basis points. At this time on Friday, the yield is at 3.976%.

Looking at the Treasury yield curve,

- The spread between 2-10 year bond yields was +8.9 basis points. At this time yesterday, the spread was +6.0 basis points.

- The spread between 2-30 year bond yields is 41.5 basis points lower. At this time yesterday, the spread was +38.4 basis points.

In the European debt market, yields on 10-year bonds were mostly lower:

Comments are closed, but trackbacks and pingbacks are open.