Militants from Hamas — classified by the vast majority of western world nations as a terrorist organization — infiltrated Israel by land, sea and air on Saturday, during a major Jewish holiday, in what was the biggest attack in decades. The incursion came hours after the Islamist militants fired thousands of rockets into Israel from Gaza.

As we deal with financial markets, we’ll focus only on the effects on the oil market, which will eventually cascade to other parts of the economy.

Neither side – nor Israel nor Palestine – is a major oil player. Israel boasts two oil refineries with a combined capacity of almost 300,000 barrels per day and has “virtually no crude oil and condensate production”, according to EIA; Palestine is of even less relevance. The situation of uncertainty and heightened geopolitical risk caused oil to spike 5.4% at the open on Monday morning to a high of $87.21 before retracing partially to the current level of $85.88, but for this conflict to have a meaningful impact on oil markets, there must be a sustained reduction in oil supply or transport.

The fear is that tensions will escalate and spread to the entire Middle East region: If western countries officially link Iranian intelligence to the Hamas attack, then Iran’s oil supply and exports face imminent downside risks. There is also the role of Iran-backed Hezbollah in Lebanon to consider, that is reported to have been engaging in small scale attacks on the north border. Iran’s oil output and exports have been rising steadily the last few years: under encouragement from the US and secret nuclear talks, Iran saw its oil exports and production grow by some 600k b/d to 3.2m of output between the end of 2022 and mid-2023 and it’s now the 5th biggest producer in the world.

There’s then the potential stop (or reversal) of the US-brokered Abraham Accords that have eased some Middle East tensions and paved the way for greater foreign investment in the region by establishing relations between Israel, UAE and Bahrain, another negative factor for the supply chain in the area: 40% of world exports goes through the Strait of Hormuz and the Suez Canal.

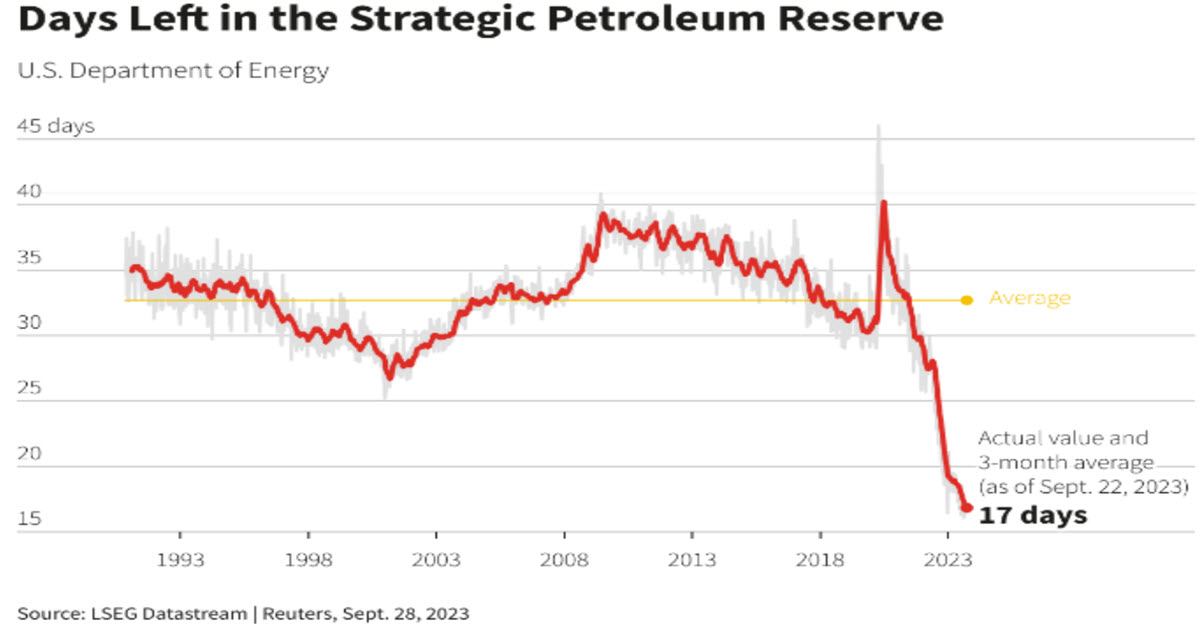

All this – according to some analysts – could lead to a premium of at least $5-10 per barrel at a time when global oil inventories are low, US SPR is at historical low levels and production cuts by Saudi Arabia and Russia will lead to more inventory draws over the next few months.

TECHNICAL ANALYSIS

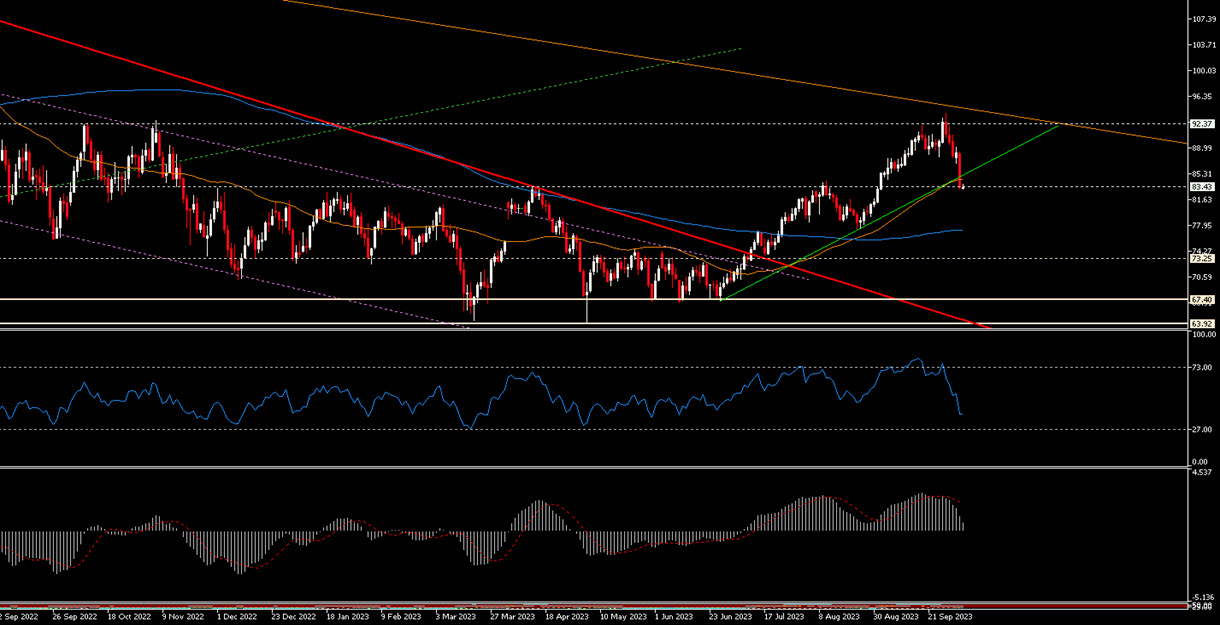

USOil closed last week 12.84% lower than the highs reached on 28 September, below the bullish trend that began on 28 June, its 50MA and the strong support in the $83.50 area. This morning it gapped up, opened above the said static level and went on to test from the bottom the uptrend lost last week: right now at $85.35 it is just above the 50MA. The RSI is below 50 (45.37) and tilted downwards, and the MACD histogram has turned negative. Were it not for the news flows, on a technical analysis base alone, this might not seem like such a solid situation. It could be a good idea to wait at least until today’s close and for the situation to clarify a little. A close today above $86 would be quite bullish and would mean a return to the bullish trendline: the next resistances would be at today’s high ($87.25) and then in the $88.25 area and finally $89. Downwards, the first important test would be the closure of the Gap, then $83.30 and then last week’s low in the $81.50 area. Much will depend on whether we really will see an escalation of tension or the world powers will be able to avoid a new pit of worry.

Click here to access our Economic Calendar

Marco Turatti

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.