US CPI KEY POINTS:

Recommended by Zain Vawda

Introduction to Forex News Trading

US headline inflation YoY in November declined to 3.1%, in line with estimates while Core CPI YoY remained steady at 4%, the U.S. Bureau of Labor Statistics reported today. The print is the lowest headline reading in 5 months and continues the downward trend of late. The concern and what is likely to keep the current Fed rhetoric going is the slight increase from the MoM print and the Core MoM figure which came in at 0.1% and 0.3% respectively.

Customize and filter live economic data via our DailyFX economic calendar

Energy costs dropped 5.4% (vs -4.5% in October), with gasoline declining 8.9%, utility (piped) gas service falling 10.4% and fuel oil sinking 24.8%. The food index increased 0.2 percent in November, after rising 0.3 percent in October. The index for food at home increased 0.1 percent over the month and the index for food away from home rose 0.4 percent.

The index for all items less food and energy rose 0.3 percent in November, after rising 0.2 percent in October. Indexes which increased in November include rent, owners’ equivalent rent, medical care, and motor vehicle insurance. The indexes for apparel, household furnishings and operations, communication, and recreation were among those that decreased over the month.

Source: US Bureau of Labor Statistics, CarbonFinance

FOMC MEETING AND BEYOND

The data out today was always unlikely to have a material impact on the Fed decision tomorrow. The data being largely in line with expectations, the slight uptick in underlying inflation may lead the Fed to push back on the growing narrative of rate cuts in 2024. Fed swaps post the data release pricing in slightly higher odds of rate cuts while futures contracts tied to Fed policy price in rate cuts as early as March 2024. Given that the Fed is expected to keep rates on hold much like the ECB, focus will be on comments by Chair Powell and any revisions to the economic outlook.

Markets will wait with bated breath to hear if there is any pushback from the Fed regarding the rate cut expectations priced in by market participants. The deviation of Fed and Market expectations will likely drive the US dollar and risk appetite following the FOMC meeting and could set the tone for the early weeks of 2024 as well.

MARKET REACTION

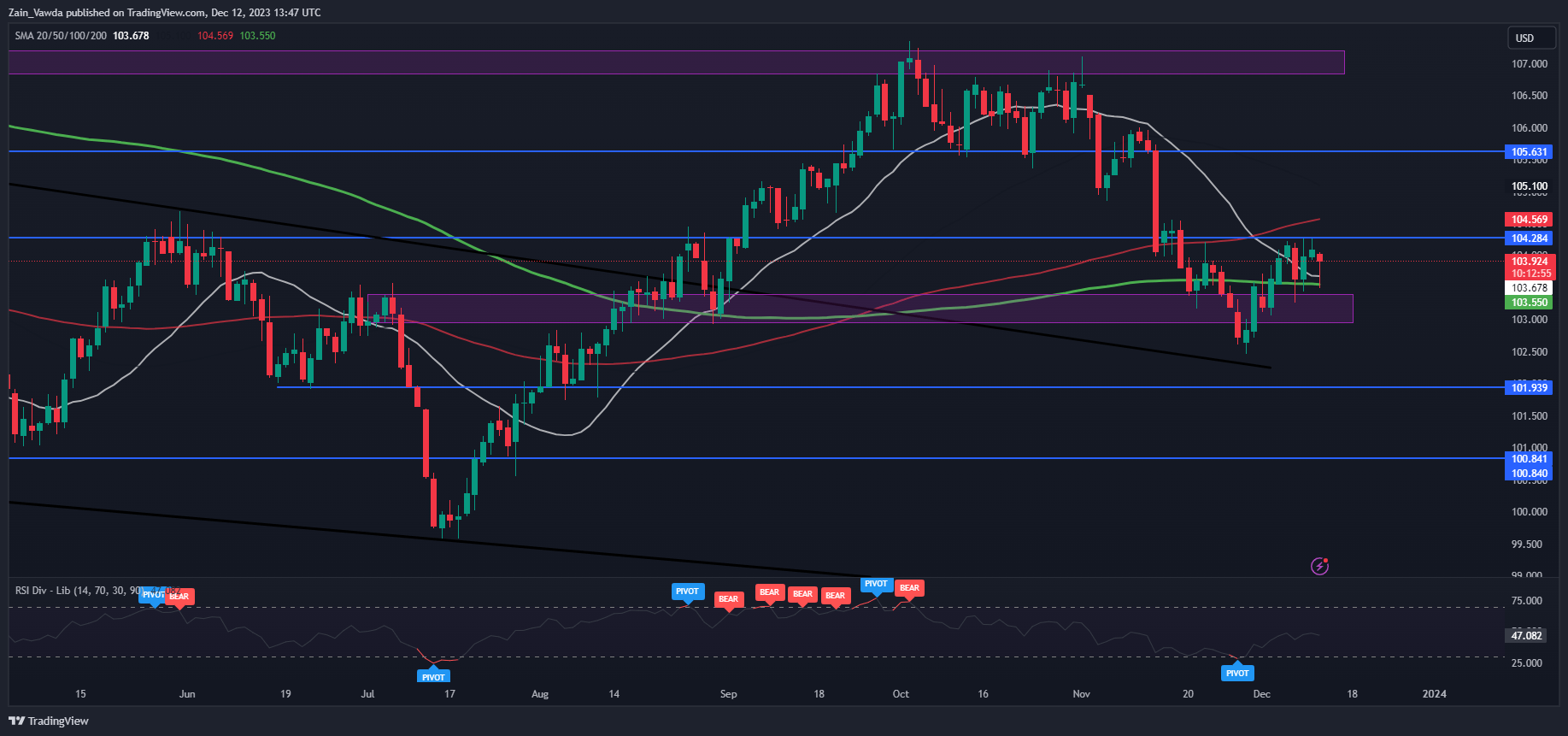

US Dollar Index (DXY) Daily Chart

Source: TradingView, prepared by Zain Vawda

The initial reaction saw the Dollar Index retreat and a rise in risk assets as markets were pricing in rate cuts as early as March 2024. However as market participants perused the data i am guessing the increase in the MoM and Core MoM prints has helped the Dollar regain some strength and risk assets surrender earlier gains. The futures contracts also repricing Fed rate cuts down to May 2024.

The DXY remains confined in a range at present between the 20 and 200-day MAs providing support and the resistance area and 100-day MA to the upside resting at the 104.30-104.50 handles. The FOMC meeting tomorrow may provide a catalyst, however this will depend on the tone and updated Fed projections and how they compare to the current market expectations when it comes to rate cuts in 2024.

Recommended by Zain Vawda

Trading Forex News: The Strategy

— Written by Zain Vawda for DailyFX.com

Contact and follow Zain on Twitter: @zvawda