Upcoming events:

- Monday: Japanese industrial production and retail sales, Chinese PMIs, German CPI, Fed Chair Powell. (Canada is on vacation)

- Tuesday: Japan Unemployment Rate, Bank of Japan Opinion Summary, Australian Retail Sales, Swiss Retail Sales, Swiss Manufacturing PMI, Eurozone Flash CPI, Canadian Manufacturing PMI, US ISM Manufacturing PMI, US Job Opportunities . (China is on vacation)

- Wednesday: Japanese Tankan index, Eurozone unemployment rate, US ADP index. (China is on vacation)

- Thursday: Swiss CPI, Eurozone Producer Price Index, US Unemployment Claims, Canadian Services PMI, US ISM Services PMI. (China is on vacation)

- Friday: Swiss unemployment rate, US NFP. (China is on vacation)

Tuesday

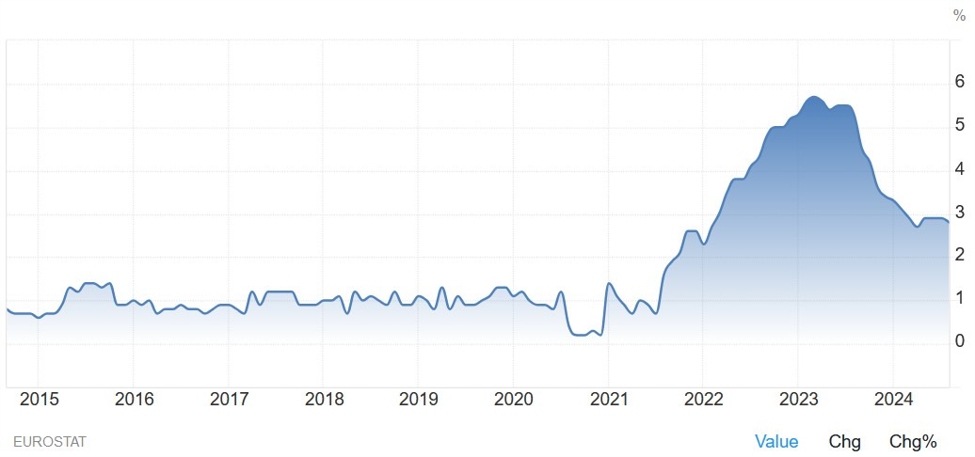

Eurozone CPI y/y is expected to be 1.9% vs. 2.2% previously, while core CPI y/y is expected to be 2.8% vs. 2.8% previously. The market has already priced in a successive 25 basis point cut in October following weak PMIs and weak French and Spanish CPI numbers last week. Expectations indicate that the European Central Bank will cut rates by 25 basis points at each meeting until June 2025.

Core consumer price index in the euro area on an annual basis

The US ISM Manufacturing PMI is expected to come in at 47.5 versus 47.2 previously. This and the Non-Farm Payrolls (NFP) report will be some of the most important economic releases this week. S&P’s global PMIs released last week showed the manufacturing index falling further in the contraction.

It is unlikely that these PMIs, and perhaps even the ISM PMIs, will have incorporated the latest Fed decision. Although ISM data is collected in the last week of the month, so there may be some improvement compared to the S&P Global report.

Given the focus on global growth following the Fed and especially the People’s Bank of China’s decisions, the market may be fine with a benign character and rejoice in a strong rebound.

The New Orders Index should be the one to watch as it should be the first to respond to recent developments. Focus will also be on the employment index ahead of the non-farm payrolls report on Friday.

US ISM Manufacturing PMI

The number of job opportunities in the United States is expected to reach 7.670 million, compared to 7.673 million previously. The last report surprised us with a significant decline. Despite this, the hiring rate improved slightly while the layoff rate remained low. It is a job market where it is currently difficult to find a job, but the risk of losing a job is also low. We will see in the coming months how the matter develops after recent developments.

Job opportunities in the United States

Thursday

Swiss CPI YoY is expected to be 1.1% vs. 1.1% previously, while CPI MoM is expected to be -0.1% vs. 0.0% previously. As a reminder, last week the Swiss Central Bank cut interest rates by only 25 basis points, bringing the interest rate to 1.00%, and said that it was ready to intervene in the foreign exchange market when necessary.

The central bank also revised its inflation forecasts lower, prompting the market to price in further interest rate cuts after December 2024. Despite this, the Swiss franc strengthened as the market likely viewed this as a weak move.

Switzerland Consumer Price Index on an annual basis

US unemployment claims remain one of the most important releases to follow each week, as they are a convenient indicator of the state of the labor market.

Initial claims remain within the 200K-260K range established since 2022, while continuing claims after a sustained rise over the summer have improved significantly in recent weeks.

Initial claims this week are expected to stand at 220k versus 218k previously, while there is no consensus on continuing claims at the time of writing although the previous release showed an increase to 1834k.

US unemployment claims

The US ISM services PMI is expected to record 51.6 versus the previous 51.5. This poll has not provided any clear indication recently because it has been ranging since 2022, and has been largely unreliable. The market may focus solely on the employment index before the non-farm payrolls report is released the next day.

“Early survey indicators for September point to an economy that continues to grow at a solid pace, albeit with a weak manufacturing sector and intensifying political uncertainty acting as significant headwinds,” S&P’s recently released Global Services PMI noted.

“The continued strong expansion in output indicated by the PMI in September is consistent with a healthy annual rate of GDP growth of 2.2% in the third quarter. But there are some warning lights flashing, particularly regarding the reliance on the services sector for growth, as Manufacturing continued to decline, and business confidence declined alarmingly.

“At the same time, a return to accelerating inflation is also being noted, suggesting that the Fed cannot shift its focus entirely away from the inflation target as it seeks to sustain economic improvement.”

Purchasing Managers’ Index (ISM) for US services

Friday

The US Nonfarm Payrolls report is expected to show 140,000 jobs added in September versus 142,000 in August and the unemployment rate to remain unchanged at 4.2%. Average hourly earnings on an annual basis are expected to be 3.8% versus 3.8% previously, while average monthly/monthly earnings are 0.3% versus 0.4% previously.

The Fed expects the unemployment rate to reach 4.4% by the end of the year with 50 basis points of easing. The unemployment rate rose in 2024 due to increased labor supply rather than more layoffs, which unemployment claims have well absorbed.

The market is placing a 53% chance of another 50 basis point cut in November, and that could rise if the non-farm payrolls report is weak. Of course, the opposite is true if the labor market report is better than expected, with a 25 basis point cut becoming the most likely move.

Unemployment rate in the United States

Comments are closed, but trackbacks and pingbacks are open.